Archive

Semicon to grow 12pc in 2008: Future Horizons

If there is going to be a global economic recession, the chip industry (but not all companies) is in the best shape possible to weather the ensuing storm!

According to Malcom Penn, CEO, Future Horizons, we are dealing with a semiconductor industry in ‘deep trauma.’ He was delivering the company’s forecast at the recently held International Electronics Forum (IEF) 2008 in Dubai, predicting a 12 percent growth this year despite signs of a wobbling US economy.

According to Malcom Penn, CEO, Future Horizons, we are dealing with a semiconductor industry in ‘deep trauma.’ He was delivering the company’s forecast at the recently held International Electronics Forum (IEF) 2008 in Dubai, predicting a 12 percent growth this year despite signs of a wobbling US economy.

Is there a need to get back to the industry basics? “Semiconductors are a peculiar business; the only sane strategy is to bet the company regularly,” once remarked Dr Gordon Moore.

Penn noted that the current industry status is somewhat confused and uncertain. Short-term issues are dominating the agenda.

Longer-term structural trends are unclear. The traditional IDMs are currently going through a mid-life ‘new business model’ identity crisis, and the start-ups are struggling to even reach critical mass! And all of this has been happening amidst intense economic uncertainty

“Now is the time for strong nerves and determination,” Penn said. According to him, the underlying industry fundamentals are sound and there is no end in sight to the ‘make-lunch-or-be-lunch’ ethos.

The emerging economies like India and China have so far been less affected by the financial market’s turbulence. In fact, the emerging and developing economies were shifting the global growth dynamics.

Chip industry in best possible shape

A forecast health warning is: IF the global economy collapses, it will take the chip market with it. However, Future Horizons feels that if there is going to be a global economic recession, the chip industry (but not all companies) is in the best shape possible to weather the ensuing storm.

The ASPs are an enigma wrapped up in riddle. The course of ASPs (like love) never runs smooth. Wobbles happen! ASPs are also the perennial (and least understood) industry wild card. ASPs are generally driven by new IC designs, and that takes time (sometimes three to four years). Post-2001, value recovery lost one generation (130nm impact). The ASP recovery ‘wobbled’ in 2007 (memory and MPU price wars). Barring a recession, Future Horizons forecasts that ASPs will recover in 2008 (it has already started).

12 percent growth likely

Future Horizons’ 2008 forecast summary and assumptions (as of May 2008) are — ‘12 percent’ growth — ’10 percent’ units / ‘2 percent’ ASP. There may be no global economic recession, although US/UK/Eurozone might wobble — which they are! No significant inventory correction will probably take place, but there are always Q4>Q1 adjustments, and there’s nothing special about that either.

There could be lower fab capacity expansion due to 2007/2008 capex slowdown, which is inevitable and irreversible. There is also a possibility of a more stable memory price erosion — which means, back to the learning vs. bleeding curve, and prices have since hardened. If the global economy holds, the 2H-08 growth will likely be strong. This, if the capacity, ASP and units are all pulling together, which is said to be happening.

Therefore, Penn feels it is too early to call for a (major) downward revision. Q1 08 was a lot stronger than conventional wisdom feared.

“That’s the rational analysis, but semiconductors aren’t rational. It could just as easily be another single digit growth year,” Penn added.

Danger signs to watch out for

So, what are the danger signs one should watch out for? These would be capacity — it is hard to see how this can spoil 2008, provided unit growth holds up, but there is a need to watch capex. Another factor is demand — the current IC unit demand is sustainable provided the economy holds up, so there is a need to watch the inventory.

Next comes the economy! The current outlook continues to be uncertain with risks all on the downside. ASPs are the key to recovery, but always the first line of defence. ASPs could still derail 2008, but the trends are encouraging.

What’s driving the market?

In semiconductor 7.0 — or the 7th decade of the transistor revolution, the same things, as always, are driving the market. These are: technology, legislation — energy saving/conservation and structural — the relentless analog to digital conversion. All of these are combining to do what the chip industry does best — enabling something that was previously impossible. Penn contends, “This industry has nowhere near run out of steam!”

New applications continue to drive the market, with automotive, industrial and medical, mobile phones, and PCs and servers, dominating. The PC market is dominating, but going nowhere fast. Mobile phones have become more interesting, but have conflicting priorities. The challenges are: how to protect the existing cost structure and subscriber base and how to add useful and affordable value-add services! Evidently, “chipset suppliers love the high end, market loves the low end.”

There is definitely an increasing automotive semiconductor content. A solid annual growth has been prediced (CAGR 2006-11) for vehicles — 5.5 percent, systems — 11.5 percent, and semiconductors — 13.3 percent. Some other new areas are motor control and energy, as well as lighting and photovoltaic, besides medical electronics. Robotics is yet another interesting area.

Key industry issues

It is clear that more chips per wafer equals less cost per chip and more transistors per die equals more functionality. Several billion transistors gives phenomenal design flexibility as well. Considering total ICs and MOS ICs, in the MOS capacity build out by technology node, there has been no change in volume ramp profile despite the hype.

As for the evolution of the technology node, definitely, 45nm is a revolutionary step from 65nm. In all likelihood, 32nm will be a natural evolutionary. However, Penn cautioned that 22nm would be another ‘difficult’ transition!

There is no doubt that 65nm will be tomorrow’s leading-edge workhorse, having the same basic Si gate/SiO2/MOSFET structure. Nevertheless, 45nm will herald a totally different structure — metal gate/high-k/thin FET/deep trench design, etc. Also, 45nm will herald a new way of system design.

Is fabless right?

Is Fablite a valid option? While there is nothing wrong with being fabless, people are just not sure whether the best starting point is being an IDM. Teamwork has to be perfectly orchestrated as competition is tough.

As for the market share dynamics, the top 10 companies (IDMs) have been losing share. Fabless share has been growing, but it is still relatively small.

Coming to the realities of the foundry market, TSMC’s lead is now unassailable. Were it an IDM, it would be No. 2, challenging Intel and passing Samsung. Moving more into design looks inevitable.

Finally, execution, and not technology, is everything! Execution has and will continue to make the difference. Applications (software) will play the role of the key differentiator as well, and it has value. Design is the means to an end, and not the end.

From the chip industry’s perspective, the electronics market was traditionally Japan, North America and Western Europe. It now encompasses the entire Asian rim, China, Eastern Europe and India. Far from maturing, the chip industry itself is still in its volatile, high-growth phase, with at least a further 20 years of strong growth in prospect. Penn said, “The underlying growth drivers for chips has never been better.”

Back to basics

We started with the need to get

back to industry basics. We end in the same way! Stick to basics like:

* Don’t invest in low cost areas just because they are cheap — they have a habit of becoming high cost tomorrow, plus the hidden extras.

* Don’t make outsourcing decisions just because they are easy — especially if there’s no way back.

* Don’t make strategic cut-backs just to trim the bottom line — some decisions, e.g., R&D, take a long time to impact, then it’s too late.

* Stop looking for high volume/high value market niches — they don’t exist, need to learn how to compete

* Do show strong leadership

* Do have a long-term plan and stick with it — even if it negatively impacts ‘the next quarter’ balance sheet

* Do show a commitment and determination to succeed

* Do stay focused and resistant to external meddling

* Do execute ruthlessly — this is the key competitive differentiator)

* Do … just do it with passion — it’s the passion that makes the difference

India's growing might in global semicon

It is no longer a secret that India is fast becoming the world’s destination, and increasingly the source too, for semiconductors. India also shows the most rapid growth potential among the BRIC countries.

Speaking at the recently held International Electronics Forum (IEF) 2008 at Dubai, organized by Future Horizons, S.Janakiraman, the outgoing Chairman – India Semiconductor Association, and President & CEO – R&D services, MindTree Ltd, touched upon India’s growing might as a being the third largest country in terms of purchasing power parity, as well as its growing presence in the global semiconductor industry.

It is no surprise that the current market drivers in India happen to be mobile phone services, IT services/BPO, automobiles and IT hardware. Add to these are the facts that India is very strong in design tools, system architecture and VLSI design, has quite strong IP protection laws, and is quite strong in concept/innovation as far as the semiconductor industry is concerned.

Testing and packaging are in the nascent stage. While India lacks a semicon wafer fab, as of now, there have been several announcements regarding solar fabs by leading firms such as Videocon, Moser Baer, Reliance, etc.

In the electronics manufacturing domain, India’s strength lies in hardware, embedded software and industrial design, OEMs, component distribution (includes semiconductor and box build), and end user/distribution channel, as well as more than moderate strength in product design and manufacturing (ODM, EMS).

India is likely to witness $363 billion of equipment consumption and $155 billion of domestic production by 2015. India’s electronic equipment consumption in 2005 was 1.8 percent. It is likely to grow to 5.5 percent in 2010 and 11 percent in 2015, as per a joint study conducted by the ISA and Frost & Sullivan.

The Indian semiconductor TAM (total available market) revenue is likely to grow by 2.5 times while the TM (total market) is likely to double revenues in 2009. The TAM is likely to grow at a CAGR of 35.8 percent and the TM is likely to grow at a CAGR of 26.7 percent, respectively, during the period 2006-09.

Telecom, and IT and office automation are currently the leading segments in both TM and TAM. Consumer segment occupies the third fastest growing area in the TM, while the industrial segment is the third fastest growing area in the TAM.

The major semiconductor categories include microprocessors, analog, memory, discrete and ASIC, while the major end use products include mobile handsets, BTS, desktops, notebooks, set-top boxes and CRT TVs.

Emerging base of EMS firms

India is also becoming an emerging base of EMS companies, thereby completing the electronics ecosystem. Five of the top 15 EMS companies globally have set up their manufacturing facilities in India. These include Celestica, Elcoteq, Flextronics, Jabil Circuit and Solectron. Two other large companies are in the process of setting up plants — Hon Hai Precision Industry and Sanmina-SCI.

Nokia has set up its manufacturing facility as well. It has invested $210 million in the plant since January 2006. The India plant has set another benchmark of achieving the fastest ramp up across all Nokia facilities worldwide. Currently, approximately 50 percent of the production from the plant is consumed domestically and the rest is exported to other countries.

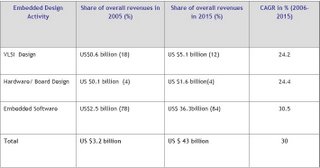

Indian embedded design industry

The Indian embedded design industry has been going from strength to strength. The recent IDC-ISA report puts revenues from India’s VLSI, board design and embedded software industry to grow to $10.96bn by 2010 from the current $6.08bn in 2007.

As of 2007, embedded has 81.1 percent share, hardware board design 6.3 percent; and VLSI design 12.3 percent, respectively. Source: ISA.

Source: ISA.

The challenges and focus areas for the embedded design industry include manpower — focusing on increasing productivity, creating readily deployable engineering workforce, and focusing on developing high-end skills.

Another area India is working on is moving up the semiconductor value chain. India is now focusing on end-to-end product development, investing in IP development, developing India specific products, and partnering with OEMs to understand the market needs.

The challenge is posed by the cost structure. India needs to better address cost management, i.e., increasing infrastructure and salary costs, as well as managing the dollar’s impact.

India design inside

Several global products have been now developed out of India. Some recent examples are: Harita Infoserve Ltd is developing interior parts and conducting computer tests on components for General Motors Corp.

Next, Ittiam’s videophone design will become almost entirely an India story: part of the chip, the product design, the software and, finally, the manufacturing also done here. Plexion Technologies has worked on the interior design and windows for a DaimlerChrysler (DCX) bus.

Quasar Innovations designed and developed a dual SIM card — PTL910 mobile phone for Primus, to be launched in the European market. The mobile phone allows the user to have SIM cards from Primus for two countries, with the phone automatically choosing the correct SIM depending on the user’s location.

Finally, MindTree itself has designed a feature rich satellite handset with mobile handset form factor for a European company.

Attractive semicon policy

India’s semiconductor policy is likely to attract investments of over $10bn. The government of India will bear 20 percent of the capital expenditure during the first 10 years for units located inside SEZs and 25 percent for those outside.

For semiconductor manufacturing (wafer fabs) plants, the policy proposes a minimum investment of $625mn. The same for ancillary plants would be $250mn.

The government’s participation in the projects would be limited to 26 percent of the equity portion. The key benefit here is the grant of the SEZ status.

India’s evolving ecosystem is driven by the bottom of the pyramid (BOP) opportunity. Tata Motors announced the now famous Nano — the Rs. 1 lakh (sub $2500) car -– said to be the world’s cheapest car. This has been indigenously developed in India, for India, by Tata Motors.

Nano has passed all mandatory crash tests and Euro IV norms. It is likely to be commercially launched in the second half of 2008.

All of these make India the most happening semiconductor and electronics destination. Don’t be surprised if companies not having an India strategy in place miss out on the action!

NAND Q108 sales falls 15.8 percent

There’s a nice report today by DRAMeXchange on the state of the NAND Flash market. It is reproduced here.

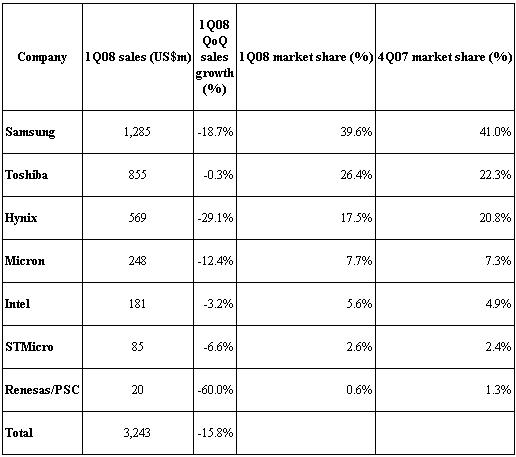

Impacted by effect of the US sub-prime mortgage loan and a slow season, oversupply of NAND Flash worsened in 1Q08. NAND Flash ASP fell about 35 percent compared to 4Q07. Although the overall bit shipment grew about 30 percent compared to 4Q07, the total 1Q08 sales of branded NAND Flash makers fell 15.8 percent QoQ to US$3.24bn.

Ranked by the overall 1Q08 sales, Samsung continues to lead. The top five NAND Flash branded makers shared 96.8 percent of the whole market share in 1Q08.

Ranked by the overall 1Q08 sales, Samsung continues to lead. The top five NAND Flash branded makers shared 96.8 percent of the whole market share in 1Q08.

Although the NAND Flash market share by sales for Samsung in 1Q08 fell to roughly 39.6 percent compared to 4Q07, Samsung continues to be the leader in branded market.

Despite the increase proportion of 51nm node production, affected by the deep decline in NAND Flash price, 1Q08 sales fell 18.7 percent QoQ to US$1.28bn.

NAND Flash market share by sales for Toshiba rose to 26.4 percent compared to 4Q07 and continued to be in the second place among the branded NAND Flash makers.

Due to Toshiba’s successful increase in 56nm node production, it was able to resist the effect of the NAND Flash price decline. However, 1Q08 sales were flat compared to 4Q07 at US$855m.

The 1Q08 market share by sales for Hynix fell to 17.5 percent, though it continued to stay at the number three spot among branded NAND Flash makers. As Hynix lowered its NAND Flash production, 1Q08 bit shipment increased only 9 percent QoQ. However, due to the fall of NAND Flash ASP at 39 percent QoQ, 1Q08 sales for Hynix fell to US$569m, or a decline of 29.1 percent QoQ.

With the ramp up of 50nm node, Micron and Intel continued to see steady growth in a bit shipment in 1Q08. However, impacted by the large decline in NAND Flash price, their 1Q08 sales fell compared to 4Q07. Micron and Intel 1Q08 sales were US$248m and US$181m, respectively, with a market share of 7.7 percent and 5.6 percent, each.

As STMicroelectronics primarily produces NAND Flash for cell phone applications, revenue for 1Q08 was not as severely impacted by the price decline. Revenue for STMicro in 1Q08 fell slightly to US$85m, or a slight decline of 6.6 percent compared to 4Q07. The 1Q08 market share by sales was 2.6 percent.

Since Renesas continued to reduce its AG-AND Flash production in 1Q08, Renesas/PSC camp sales fell roughly 60 percent compared to 4Q07 with a market share of 0.6 percent.