Archive

Global semiconductor market for PMPs likely to decline at -9.1pc CAGR through 2013

The worldwide semiconductor market for portable media players (PMPs) is poised to drop significantly from $7.5 billion in 2008 to $4.6 billion in 2013, representing a negative compound annual growth rate (CAGR) of -9%, according to a new forecast from IDC.

A mature market, the economic slowdown, growing similarity with mobile phones and mobile Internet devices (MIDs), and inevitable cannibalization all contribute to the shrinking semiconductor opportunity in PMPs. Additionally, PMPs will no longer be the largest market for NAND flash memory.

While revenue for most of the semiconductor components will decline in line with the total decline in PMP unit shipments, wireless connectivity semiconductors will exhibit modest growth, driven by the increase in attach rate for FM, WLAN, and Bluetooth radios.

“As PMPs have grown in capabilities, the dividing line has blurred between multimedia phones and MIDs,” said Ajit Deosthali, research manager for Short Range Wireless Semiconductors at IDC. “Moving forward, one should expect the semiconductor players to focus on the larger multimedia phones and growing opportunity in MIDs.”

IDC’s study, Worldwide Portable Media Player Semiconductor 2009–2013 Forecast provides an analysis of the worldwide semiconductor market for PMPs by device type, from 2009 to 2013.

The study also forecasts the semiconductor bill of materials for audio-only and video-capable PMPs, and the PMP NAND flash revenue and shipments by capacity.

Indian design services to hit $10.96bn by 2010

This is a continuation of my previous blog on the Indian design services segment.

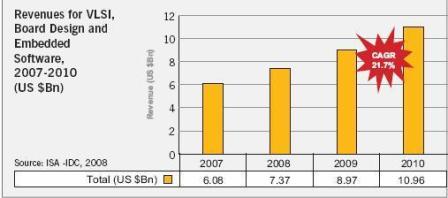

Revenues for the VLSI, board design and embedded software market in India are likely to touch US $10.96bn in 2010, according to an ISA-IDC study titled India Semiconductor and Embedded Design Market, 2007-2010. This market will grow from US $6.08bn in 2007 to US $7.37bn in 2008, on to US $8.97bn in 2009, respectively.

Revenues for the VLSI, board design and embedded software market in India are likely to touch US $10.96bn in 2010, according to an ISA-IDC study titled India Semiconductor and Embedded Design Market, 2007-2010. This market will grow from US $6.08bn in 2007 to US $7.37bn in 2008, on to US $8.97bn in 2009, respectively.

The total design services market in India is said to have grown at 21 percent year on year (y-o-y), as against a global growth of 6 percent y-o-y. According to Kapil Dev Singh, Country Manager, IDC (I) Ltd, the impending recession in US and sheer volume of work from US will put pressure on man-month rates and they will increase marginally. Currently there are close to 200+ companies active in India.

Touching upon the market trends for 2007 in the India semiconductor and embedded design market, he added that India will continue to be the preferred destination of choice for companies interested in embedded design and development.

There will also be an increased emphasis on IP development, as third-party design services companies look to move up the value chain. Next, localization of products design and manufacturing from India will drive significant investments by product and design services companies leading to a further fueling of growth.

However, he cautioned that the industry will continue to face significant challenges in managing the demand and workforce churn. The industry will also have to constantly evolve, upgrade and innovate, while keeping the costs down in order to stay cost competitive in the global market. Future trends in this industry will further witness the increasing proximity between the third-party service providers and OEMs for end-to-end product design.

Indan design services industry snapshot

The Indian VLSI design services contributed approximately 13 percent to the overall revenues and 11 percent to overall workforce. There has been an increase in consumer and portable/wireless segment, that has indirectly contributed to the growth of the VLSI design service industry in India. Spec to tape-out designs are gradually increasing as well, largely contributed to by the captive units. The IP development will continue to grow steadily during the forecast period.

The Indian hardware/board design industry contributed to 7.2 percent of the overall technical workforce in the design services industry. The trend of VLSI design houses transforming into one-stop design houses has increased the activity in the hardware/board design area. Growth is likely to come from consumer electronics and portable/wireless product segment in 2008. Product development activities for the Indian market will further boost growth.

The Indian embedded software industry is by and large, the most significant contributor. Embedded software contributed approximately 81 percent to the overall design services revenues and 82 percent to the overall workforce. Having a local manufacturing ecosystem will boost this segment with end-to-end product development and roll-out happening from India. Singh said that middleware/embedded applications along with testing will drive the growth in the market.

Two vectors for industry

Singh added that there were two vectors that the industry could go to. One, focus on export revenue and go closer to markets — to their customers’ markets and be part of product development. And two, focus on product development, as it would drive semiconductors and embedded design. He termed the growth achieved in the last three decades as version 1.0 and said India was ready to move on to version 2.0 in the coming years.

In version 2.0, the dynamics between the semiconductor industry ecosystem players would be transformed in the coming years. Also, there will be a disruption, which will see the entities shift their strategies, align and engage with each other within this ecosystem in a manner that will take them up one level in the overall product value chain.

E.K. Bharat Bhushan, director general, STPI, commented: “India is a very important destination. A wide range of design activities are now going on here. Semiconductor design has made rapid strides. India currently has strengths in areas such as IP development, and core advantages in terms of talent and local domestic market.”

Indian design services to cross $7.37bn in 2008

The Indian semiconductor and embedded design services market has grown consistently over the last five years and market is likely to cross the US$ 7.37 billion in 2008.

This was the key finding of the “India semiconductor and embedded design service industry (2007-2010): Market, technology and ecosystem analysis”, a study jointly released today in Bangalore by the India Semiconductor Association (ISA), and IDC (India) Ltd.

Some key findings of this comprehensive report include:

* The total design market in India for 2007 was estimated at US $6 billion. Eighty-one percent of the revenues were in the area of embedded software, followed by VLSI design (13 percent) and hardware/board design (6 percent).

* The total workforce employed in the design services industry in India was estimated at 130,000 in 2007.Of this the bulk of the jobs were in embedded software 82 percent followed by VLSI design (11 percent) and hardware/board (7 percent).

* The industry was estimated to grow at a CAGR of around 21.7 percent between 2007-2010.

* The geographical focus of the industry indicates that US has a share of 70 percent; Europe at 30 percent; and the emerging economy is that of Japan.

Key factors that determine the growth of the design sector in India are: the growing expertise and capabilities in complex end-to-end design; strong IP development and talent. The Indian domestic market is one of the fastest growing in Asia as well as globally.

Commenting on the Indian design market, Poornima Shenoy, president, ISA, said: “The Indian semiconductor design industry, with over 200 companies, is on a strong growth trajectory. Our growth is nearly 22 percent which is three times the global growth rate of around 7 percent. We are looking eastward for business and collaboration heralding a new era in the future of the sector.”

Announcing the findings of the ISA-IDC report, Kapil Dev Singh, added: “The Indian semiconductor and embedded design services market has grown consistently over last the five years and market is expected to cross the US$ 7.37 billion in 2008. The domestic semiconductor and embedded design services industry is all set to enter a new phase -– Ver 2.0, following on from where Ver 1.0 left off. To achieve this next phase of growth, the industry needs to focus on the availability of quality manpower, higher productivity and more value creation.”

IDC's semicon predictions and top 10 vendors

Looks like a season of predictions in semiconductors. Just a few weeks back, I was looking at IC Insights’ top 20 global semicon rankings by sales. And now, we have IDC’s list of the top 10 vendors by revenue, along with predictions of its own. Let’s look at the table.

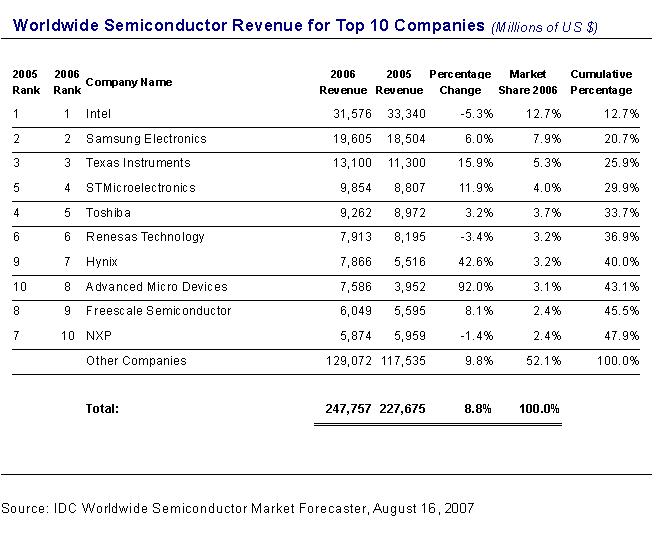

According to IDC’s table, Intel, Samsung and Texas Instruments held on to the number 1, 2 and 3 positions respectively, with TI showing the highest growth percentage in revenue among the top three leaders.

With the exception of Intel, Renesas, and NXP, all other vendors in IDC’s 2006 top 10 ranking showed positive growth. Hynix grew at an amazing rate of 43 percent over the same period thanks to the company’s growing position in DRAM and NAND.

Now, if we look back at IC Insights’ ranking from a few weeks ago, I find some differences. First, the similarity — The top three — Intel, Samsung and TI, retain their positions in both tables!

However, in IC Insights’ table, ST and Toshiba exchanged the next two positions, as did Hynix and TSMC, while Renesas was at no. 8! Freescale dropped from no. 9 to no. 16, while Sony, NXP and NEC gained one place each. Infineon climbed back up to no. 12, from no. 16, while Qualcomm occupied the no. 13 position, up from no. 17. AMD dropped two positions, from no. 13 to no. 15.

In IDC’s table (by semicon revenue), STMicroelectronics, Toshiba, Renesas, Hynix, AMD, Freescale and NXP occupied positions 4th to 10th, respectively. IDC has made some predictions as well. These include:

Outlook for 2007

* Demand for semiconductors is centered on the big three segments: PC and mobile phone unit volume is steady, led by emerging regions and low-end products. Consumer demand is lackluster, but excess inventory has subsided and IDC expects the design momentum to lead to healthy volume growth during the holiday season.

* DRAM and NAND are experiencing much lower revenue outlook this year following the severe price correction in the first half of 2007.

* Microprocessor market remains flat this year.

Long-term trends

* Emerging regions will boost semiconductor volume growth.

* Multimedia-rich mobile phones continue to drive semiconductor content and demand for processing, memory consumption, and power management.

* Personal computing further migrates toward mobility and low-priced form factors.

* Video processing proliferates across multiple consumer electronic segments, resulting in strong growth for semiconductor suppliers.

* Semiconductor connectivity technologies drive new usage models across device segments.

* Growth in personal content implies increasing need for storage, including NAND.

By the way, IDC’s Worldwide Semiconductor Market Forecaster predicts that the 2007 revenue slowdown in the worldwide semiconductor market will make way to a healthier 2008!

The worldwide semiconductor market will grow at a conservative rate of 4.8 percent in 2007, compared to 8.8 percent in 2006. IDC expects growth to resume at 8.1 percent in 2008 based on the current outlook. Interesting days ahead in semicon!