Archive

Turnaround finally in global mobile phone market?

Late this week, there were three reports on the global mobile phone market!

First, IDC, which says that the mobile phone market had turned a corner in Q3, and more gains are likely in Q4-2009.

Then, ABI Research pointed out that the outlook for mobile phones continue to improve — with 291.1 million mobile handsets shipped in Q3-2009 — a contraction of 6.5 percent.

Finally, Strategy Analytics also reported that global mobile handset shipments fell 4 percent year-over-year, to reach 291 million units in Q3 2009.

One other interesting aspect — while the top five vendors — Nokia, Samsung, LG, Sony Ericsson and Motorola — either held on or lost a small amount of their market share, Apple has increased its share to 2.5 percent — a figure common with both ABI Research and Strategy Analytics.

Well, all of this can only be good news for the global technology industry as well as the global mobile phone market — both of whom have had to face the wrath of probably the longest ever recession! Perhaps, it is also a good news for the mobile phone semiconductor market as well!

ISA Vision Summit 2009: Local products, emerging opportunities!

The first session on day 1 of the ISA Vision Summit 2009 focused on local products and emerging opportunities in India, especially in healthcare, automotive electronics and mobility. It was great to see companies present solutions developed for India, by Indians. If earlier, it used to be “made by the world for India,” today, it has changed to “made by the world, in India.” This focuses highly on India’s well known strength in design services.

In the picture, you can see Ajay Vasudeva, Head R&D, Nokia India, making a point, with Prof. Rajeev Gowda, IIM-Bangalore, Ashish Shah, GM, GE Healthcare, and Dr. Aravind S. Bharadwaj, CEO, Automotive Infotronics, listening very attentively.

In the picture, you can see Ajay Vasudeva, Head R&D, Nokia India, making a point, with Prof. Rajeev Gowda, IIM-Bangalore, Ashish Shah, GM, GE Healthcare, and Dr. Aravind S. Bharadwaj, CEO, Automotive Infotronics, listening very attentively.

In his opening remarks, Prof. Rajeev Gowda, IIM-Bangalore, said: “As the world is in recession, we are still cheerful, and we are still growing.” He called upon the industry to focus on healthcare, which is an area where work is going on. Agriculture is yet another area to look at! According to him, Bangalore had become an IT center, it had yet to become a knowledge center. “As an industry, think about reaching out to colleges, and get people to think innovatively and creatively,” he added.

Dr. Aravind S. Bharadwaj, CEO, Automotive Infotronics Pvt Ltd, a a joint venture between Ashok Leyland and Continental AG, in his presentation, highlighted that infotronics for automotives is an opportunity for India. He added that the infotronics content in automotives was growing, and is likely to touch around 40 percent by 2010. In India, the auto industry was growing at a CAGR of 11.4 percent, and auto electronics was growing at a CAGR of 21 percent.

What is the India advantage here? “We definitely have a high level of expertise. India can also become an automotive embedded powerhouse,” he said.

Dwelling on the current trends in automotive electronics in India, he said that there has been an increase in demand by customers for technically advanced in vehicles. Also, there are strict emission and safety regulations in place. Some other trends include the increase in automotive exports, and fuel economy in Indian driving conditions.

Dr. Bharadwaj cited the example of the fleet management telematics solution at the Koyambedu bus terminus in Chennai. He added that embedded automotive applications will dominate the future automotive applications.

Healthcare market to explode!

Ashish Shah, General Manager, GE Healthcare Global Technology Organization, India, said that two sectors will undergo tremendous growth in India: healthcare and energy, and added that the country is now ready for growth. He highlighted the fact that about 20 percent of GE’s engineers were Indians, thereby indicating a huge talent pool within the country itself.

The drivers for Indian healtcare market include: medical tourism: About 175,000 foreign nationals; up 25 percent; huge investments: government spending up 1-2 percent of GDP; disease patterns: such as lifestyle diseases; and increased spending in healthcare.

The bottom line is that growth is for real! The Indian healthcare market is about to explode,” said Shah.

Shah displayed an ECG, the MAC 400, which has been developed for India. While the company shipped 3,600 units last year, and of these, about 500 units in India, GE projects selling 10,000 units during this year. The selling price of this device is an affordable $700. GE is also making maternal infant products, as well as x-ray programs. It is also developing an MRI application, which would not require the injecting of a contrast agent, thereby, leading to 50 percent savings!

In his presentation, Ajay Vasudeva, Head R&D, Nokia India, focused on the tipping point for mobility today. More people have access to a mobile phone than a PC, and most use it to access the Internet.

He highlighted some of the applications Nokia is developing, such as those for mobile rural/irrigation applications, mobile banking and NFC (near fied communications), and mobile healthcare and diabetes checking — all using the mobile phone! Livelihood, such as agriculture, and life improvement, such as education, services are highly relevant in India. Of course, entertainment has the widest appeal!

Vasudeva concluded by remarking, “Together, let’s create devices, products, services and solutions, that can change peoples’ lives.”

In his concluding remarks, Prof. Rajeev Gowda, session moderator, called upon India to devise policies on e-waste, and to think about how can we convert semiconductor waste into energy.

NXP India's Rajeev Mehtani on top trends in global/Indian electronics and semicon!

When a new year approaches, we start analyzing the year gone by and try to gauge what could happen in the coming year. This really holds true, as far as the technology industry is concerned.

When a new year approaches, we start analyzing the year gone by and try to gauge what could happen in the coming year. This really holds true, as far as the technology industry is concerned.

It’s been a week since I’ve been mulling over these myself, especially, pondering over developments in the global semiconductor and electronics industries, as well as what could happen in India during 2009. Well, lots will happen, and I can’t wait for the new year to start!

I caught up with Rajeev Mehtani, vice president and managing director, NXP Semiconductors, India, and discussed in depth about the trends for 2009. Here’s a look at that discussion.

INDIA — ELECTRONICS & SEMICONDUCTORS

1. The DTH story will continue to increase in India with companies such as Tata Sky, DISH TV, BIG TV, etc., gaining market share. Owing to these challenges, there would be significant consolidation among the cable operators. Digitalization will also be seen in 2009.

2. The slowdown will affect growth across all sectors. Our view is that LCD TVs as well as STBs will continue to grow.

3. The year 2009 will witness e-commerce revolution and the RFID sector will grow at a 40-50 percent clip. The government has been sponsoring a lot of projects, which include RFID in the metros, e-passport cards and national ID cards. By mid-2009, we can expect a mass deployment of these projects as well as micro payments.

4. Manufacturing in India will continue to grow; EMS or OEMs, such as Samsung, Nokia, Flextronics, etc.

5. There could be a move from services to products in electronics and semiconductor spaces. The number of funded startups has grown significantly over the last years and more and more ideas are coming on the table.

6. The solar/PV sector will grow in India. High entry cost of capital for panels will be a barrier for this sector. Government enhancement is necessary. India will be different than other countries as people won’t push energy back into the grid; it will be used more for household consumption. The India grid is unstable. Tracking it requires a lot of expensive electronic switching. Solar deployment could be at the micro level, and also community level, where it makes more sense.

7. The startups in India are mostly Web 2.0 based, although there aren’t many hardware startups.

GLOBAL — ELECTRONICS & SEMICONDUCTORS

1. The semiconductor industry is truly global, That is mostly because it is a very expensive industry.

2. Things are a bit murky in the semiconductor industry. It would probably be dipping 10-15 percent next year.

3. Globally, energy management and home automation will start to take off in 2009. Satellite broadcasters will also continue to gain more strength.

4. On a worldwide scale, 3G will win. You will have 3G phones, and you’d add LTE to those. India is slightly different. Only 20 percent of Indian households are ready for broadband access. In India, WiMAX could be a way to have wireless broadband at home.

5. Industries moving to 300mm fabs will be making up only 20-25pc of the market. Not many need 45nm or 40nm chips. People will question any major capex, until there’s a big return and wait for recession to end. The bright spot is solar!

6. The fabless strategy would be the only way to go forward. While MNCs with fabless strategy are present in India, Indian startups in this space are quite few.

Why compare, ape or even try to 'kill' iPhone?

The Apple iPhone and now, the iPhone 3G, has caught everyone’s imagination. You come across reports such as top alternatives to the iPhone. Or, about companies launching new mobile phones and those inadvertently getting compared to the Apple iPhone! Or even, reports of how newer mobile phones could ‘kill’ the iPhone!

Quite hilarious and nothing new here! It has happened quite a few times in the past!

Nothing will “kill” the Apple iPhone, and at least, not so fast! Nor is any iPhone killer anywhere close in sight!!

Public memory is indeed short!!

Quite a few years back, Apple launched the very colorful iMacs! All of a sudden, there was a slew of similar PCs with color or ‘color monitor covers’. Back then, Apple had rewritten the rules of the PC industry in some manner, besides re-invigorating the Apple brand itself.

Next came the iPod, and later, colorful iPods. It led to a surge in media players, MP3/MP4 players, etc., from other several players as well. Not to speak of the iPod giving birth to a whole new range of Mac accessories! The iPod continues to be in the news, and successfully so!

A similar thing has happened this time!

With the advent of the iPhone, and now iPhone 3G, we sometimes see reports of how the iPhone could influence the memory market! Or, how the impact of Apple’s iPhone 3G has been minimal on the chip market. Or, how it’s just one item in a very large and complex mix of products.

Or, how the Apple Safari works so very well on the iPhone. Or, how the Accelerometer allows viewing pictures in any way you wish. Or, how you can do wireless social networking! Or, how the mobile OS battle has heated up! Or, how the App Store has so many wonderful applications for the iPhone!

Has creativity gone out of the window?

My question is: Who has stopped the others from doing things differently? No one!

Public memory is indeed short! So many were quick to run down the Apple Newton, which was clearly ahead of its time. However, it led to the advent of a host of PDAs, though many may disagree with me on this thought, and so be it.

The first mistake that people commit are either comparing their products or the phone they buy with the iPhone! Why are you even comparing?

Apple has been very creative, so why is that so difficult to accept? Try and do better than Apple, if possible.

Perhaps, it would be better to concentrate on developing newer and better phones and other devices with even better features, rather than either comparing with or aping the iPhone, or even trying to beat it or ‘kill it’! Where’s the need?

Remember that Nokia phone model with changeable covers in 2000? Or, the Sony Ericssion T68? Likewise, each product is unique, has its deserved place in the sun, and also has its own shelf life.

The iPhone is a wonderful benchmark, for now. Do remember that the mobile phone design bar has constantly and consistently been raised.

Am sure, it would be no different this time!

No one told you that should NOT buy any other mobile phone. Did Apple ask you to buy the iPhone? It’s your choice! I don’t even have one!!

Alongside, we are also seeing a whole range of mobile phones, which are said to be good alternatives to the iPhone! Maybe they are.

Till then, Apple and iPhone deserve their place in the sun, make no mistake! Isn’t everyone trying to “ride” the iPhone wave anyway? That’s proof of life!

India's growing might in global semicon

It is no longer a secret that India is fast becoming the world’s destination, and increasingly the source too, for semiconductors. India also shows the most rapid growth potential among the BRIC countries.

Speaking at the recently held International Electronics Forum (IEF) 2008 at Dubai, organized by Future Horizons, S.Janakiraman, the outgoing Chairman – India Semiconductor Association, and President & CEO – R&D services, MindTree Ltd, touched upon India’s growing might as a being the third largest country in terms of purchasing power parity, as well as its growing presence in the global semiconductor industry.

It is no surprise that the current market drivers in India happen to be mobile phone services, IT services/BPO, automobiles and IT hardware. Add to these are the facts that India is very strong in design tools, system architecture and VLSI design, has quite strong IP protection laws, and is quite strong in concept/innovation as far as the semiconductor industry is concerned.

Testing and packaging are in the nascent stage. While India lacks a semicon wafer fab, as of now, there have been several announcements regarding solar fabs by leading firms such as Videocon, Moser Baer, Reliance, etc.

In the electronics manufacturing domain, India’s strength lies in hardware, embedded software and industrial design, OEMs, component distribution (includes semiconductor and box build), and end user/distribution channel, as well as more than moderate strength in product design and manufacturing (ODM, EMS).

India is likely to witness $363 billion of equipment consumption and $155 billion of domestic production by 2015. India’s electronic equipment consumption in 2005 was 1.8 percent. It is likely to grow to 5.5 percent in 2010 and 11 percent in 2015, as per a joint study conducted by the ISA and Frost & Sullivan.

The Indian semiconductor TAM (total available market) revenue is likely to grow by 2.5 times while the TM (total market) is likely to double revenues in 2009. The TAM is likely to grow at a CAGR of 35.8 percent and the TM is likely to grow at a CAGR of 26.7 percent, respectively, during the period 2006-09.

Telecom, and IT and office automation are currently the leading segments in both TM and TAM. Consumer segment occupies the third fastest growing area in the TM, while the industrial segment is the third fastest growing area in the TAM.

The major semiconductor categories include microprocessors, analog, memory, discrete and ASIC, while the major end use products include mobile handsets, BTS, desktops, notebooks, set-top boxes and CRT TVs.

Emerging base of EMS firms

India is also becoming an emerging base of EMS companies, thereby completing the electronics ecosystem. Five of the top 15 EMS companies globally have set up their manufacturing facilities in India. These include Celestica, Elcoteq, Flextronics, Jabil Circuit and Solectron. Two other large companies are in the process of setting up plants — Hon Hai Precision Industry and Sanmina-SCI.

Nokia has set up its manufacturing facility as well. It has invested $210 million in the plant since January 2006. The India plant has set another benchmark of achieving the fastest ramp up across all Nokia facilities worldwide. Currently, approximately 50 percent of the production from the plant is consumed domestically and the rest is exported to other countries.

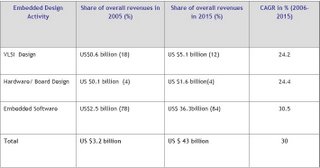

Indian embedded design industry

The Indian embedded design industry has been going from strength to strength. The recent IDC-ISA report puts revenues from India’s VLSI, board design and embedded software industry to grow to $10.96bn by 2010 from the current $6.08bn in 2007.

As of 2007, embedded has 81.1 percent share, hardware board design 6.3 percent; and VLSI design 12.3 percent, respectively. Source: ISA.

Source: ISA.

The challenges and focus areas for the embedded design industry include manpower — focusing on increasing productivity, creating readily deployable engineering workforce, and focusing on developing high-end skills.

Another area India is working on is moving up the semiconductor value chain. India is now focusing on end-to-end product development, investing in IP development, developing India specific products, and partnering with OEMs to understand the market needs.

The challenge is posed by the cost structure. India needs to better address cost management, i.e., increasing infrastructure and salary costs, as well as managing the dollar’s impact.

India design inside

Several global products have been now developed out of India. Some recent examples are: Harita Infoserve Ltd is developing interior parts and conducting computer tests on components for General Motors Corp.

Next, Ittiam’s videophone design will become almost entirely an India story: part of the chip, the product design, the software and, finally, the manufacturing also done here. Plexion Technologies has worked on the interior design and windows for a DaimlerChrysler (DCX) bus.

Quasar Innovations designed and developed a dual SIM card — PTL910 mobile phone for Primus, to be launched in the European market. The mobile phone allows the user to have SIM cards from Primus for two countries, with the phone automatically choosing the correct SIM depending on the user’s location.

Finally, MindTree itself has designed a feature rich satellite handset with mobile handset form factor for a European company.

Attractive semicon policy

India’s semiconductor policy is likely to attract investments of over $10bn. The government of India will bear 20 percent of the capital expenditure during the first 10 years for units located inside SEZs and 25 percent for those outside.

For semiconductor manufacturing (wafer fabs) plants, the policy proposes a minimum investment of $625mn. The same for ancillary plants would be $250mn.

The government’s participation in the projects would be limited to 26 percent of the equity portion. The key benefit here is the grant of the SEZ status.

India’s evolving ecosystem is driven by the bottom of the pyramid (BOP) opportunity. Tata Motors announced the now famous Nano — the Rs. 1 lakh (sub $2500) car -– said to be the world’s cheapest car. This has been indigenously developed in India, for India, by Tata Motors.

Nano has passed all mandatory crash tests and Euro IV norms. It is likely to be commercially launched in the second half of 2008.

All of these make India the most happening semiconductor and electronics destination. Don’t be surprised if companies not having an India strategy in place miss out on the action!