Archive

Japanese quake and tsunami — too devastating to watch on TV!

I’m shocked — seeing the devastating images on TV from the Japanese earthquake and tsunami! The images on TV from Japan’s earthquake and tsunami are just too depressing! I am really worried for some of my friends from that part of the world! Shinpai da!!

Japan's earthquake and tsunami: Courtesy: STAR News, India.

It is being reported on TV that the quake has shifted the earth off Japanese coast by 8cm (or is it inches?). There are likely to be severe aftershocks. The official Japanese death toll is currently 801, with thousands missing. There are threats of a nuclear meltdown. Over 200,000 people have so far been evacuated from the area.

The natural disaster is unprecedented, says the Japanese prime minister. The earthquake has knocked out electric power to an estimated over 6 million homes. Sendai is among the worst affected areas. There is widespread flooding and destruction in Natori city, Miyagi prefecture. There are concerns of fuel and food shortages in Japan as well.

NHK has been showing devastating images of the tsunami that has struck Japan post the earthquakes. Staffers at Fukushima Daichi plant are still working to lower the reactor temperatures. About 9,500 are said to be mising at Minamisanriku. The world is said to be already mobilizing to help victims of Friday’s 8.9-magnitude earthquake that unleashed a devastating tsunami on Japan, reports CNN.

According to IHS iSuppli, the Japanese DRAM manufacturing accounts for 10 percent of the global supply based on wafer production. The two major DRAM fabs in Japan, operated by US based-Micron and Japan’s Elpida, have not been directly affected, according to preliminary indications from IHS iSuppli contacts. Japanese companies, mainly Toshiba Corp., account for 35 percent of global NAND flash production in terms of revenue.

The more important impact may be on Japan’s production of components for LCD panels. Japan accounts for a very high share of components uses in LCD panels and LCD-based products, including glass, color filters, polarizers, cold cathode fluorescent lamps (CCFLs) and light-emitting diodes (LEDs).

I have contacted the few friends I have in Japan, one, an ex-Global Sources employee, and the rest from the Japanese semiconductor/electronics industry. Hope all of them are safe and sound. Hope to be back with more!

PS: I just heard from my friend, Yoshio Washizu. An ex-Global Sources colleague, he lives in southern Japan, in Kyushu Island, and is not affected by the monster earthquake.

He says: “What happened in the eastern Japan is simply unreal. I have to go to Tokyo later this week and stay there until Sunday, I am not so keen on doing so, though. The earthquake badly shook Tokyo as well. And it is forecasted there is a 50 percent chance of us having the aftermath in the next five days. So I’m a little bit uncomfortable.”

Stay safe, my friend!

It’s Q1 seasonal slowdown, and yearly time for denial!

This is a summary by Malcolm Penn, CEO, Future Horizons. For those who wish to know more, please get in touch with me or Future Horizons.

Malcolm Penn, CEO, Future Horizons.

December’s WSTS results were as boring as they were predictable, with no serious data revisions (thankfully) and the results right where we expected. December’s year-on-year IC unit growth was 8.9 percent that, with the 3.5 percent growth (yes GROWTH) in ASPs, yielded a respectable double-digit value growthof 12.8 percent. And this, on the back of a weak Q4 memory market that saw ASPs fall 13.1 percent vs Q3-10!

The yearly growth vs 2009 weighed in at 31.8 percent, hitting $298.3 billion, just shy of the elusive $300 billion threshold. The market is right where we said it would be at our recent 2011 Forecast seminar; we reiterate our position that 2011 will be a good year for the industry. Choppy first-half waters for sure, but watch out for a whopping 2H-11 ricochet.

Connectors are up as well

It is not just semiconductors that are off to a good start. The connector industry is tight as a drum too. Orders in December 2010 were up 13.3 percent versus December 2009, with full year orders up 29.3 percent on 2009, down sequentially 11.1 percent from November 2010. The comparable data for sales was plus 18.7percent, plus 28.4 and minus 13.7 percent.

The December connector book-to-bill ratio was 1.01, unchanged from November. This industry still publishes orders and book-to-bill data by the way, unlike the chip industry which very foolishly stopped publishing this several years ago. All this in the seasonally slow first quarter of the month, yet few people believe there is a supply problem in prospect. Just as this time last year, industry denial is rampant, way beyond reasonable caution and ignoring the underlying trends.

Strong demand for mobile, server and graphics DRAM

We estimate that the worldwide growth rate for PCs in 2011 will be a healthy 10 percent, with 3.9GB the average DRAM content per box. New capacity and die shrinks are putting near-term pressure on over-supply and pricing but there are now move afoot from Elpida and others to start raising prices.

Where they can, to gain a price advantage, DRAM vendors are actively adjusting their supply in favour of mobile from commodity DRAM, given the current strong demand in the smartphone and tablet PC markets, with a 1GB per box average DRAM content.

Server demand continues to be the other star segment, not just in unit demand but in content per box as well, estimated to average around 30GB in 2011. This will drive a 50 to 60 percent increase in server DRAM demand. Finally in graphics demand for specialty DRAM is also very strong, driven by the rapid take off of3D-TV and continuing strong growth in Blue-Ray DVD.

The overall DRAM industry is thus gradually diversifying from manufacturing mainly commodity DRAM to diversified products such as mobile DRAM, serverbasis DRAM, specialty DRAM and graphic memory.DRAM vendors however are faring mixed fortunes, with Elpida and Hynix having the worst net cash positions with barely enough cash to cover their short-term debt.

The Taiwanese vendors find themselves stuck in a technology trap, unable to invest in the immersion technology needed to break through the 5*nm node, meaning that in the absence of a good market uptick to improve cash flow and profits, a shake out in the DRAM supply base seems unavoidable.

Read more…

Top 20 global semicon suppliers of 2010!

I’ve just received this report from iSuppli, which says that the global semiconductor revenue expands by record margin in 2010 — to $304 billion in 2010, up from $229.5 billion in 2009. This represents growth of 32.5 percent for the year! Fantastic!!

This growth is said to be courtesy of a boom in DRAM and NAND sales benefiting memory suppliers. One hopes the semicon industry turns in an equally better performance in 2011. That’d be just great!

In the meantime, I’d like to share with you iSuppli’s preliminary ranking of the Top 20 semiconductor suppliers in 2010.

Top 20 semiconductor suppliers of 2010: Source: iSuppli, USA.

As per iSuppli, Marvell is likely to achieve organic revenue growth of more than 43 percent and jump five places to the No. 18 spot in 2010.

Qualcomm and AMD, and Sony have experienced revenue growth notably less than the overall market. Therefore, they will likely slip three to four positions in the rankings in 2010.

After a number of years of dramatically outperforming the market, Taiwan’s MediaTek fell back to earth in 2010, as it will barely achieve revenue growth at 1.2 percent, the only company among the Top 20 to not achieve a double-digit increase. The company is likely to slip to No. 19 in the rankings, down from No. 16 place in 2009.

Only one company is at risk of dropping out of the list of 20. iSuppli projects that nVidia will retain its ranking at No. 20. However, ROHM Semiconductor is competing for the final slot among the Top 20 and the final outcome should be very close.

I hope to get into a conversation with iSuppli regarding the top 20 semicon suppliers.

Why has the semicon equipment bubble really burst? – II

Here’s the concluding part of my discussion with Dr. Robert Castellano of The Information Network, from New Tripoli, USA.

Repercussions of a deteriorating semiconductor industry

I asked Dr. Castellano regarding the repercussions of a deteriorating semiconductor industry.

He said that the semiconductor equipment industry seems to be in serious trouble. There could possible be little growth in 2011, and the how is that there will be sufficient pushouts in equipment that revenues are moved to 2011 from 2010.

Dr. Castellano said: “We warned two months ago about pushouts, and today, Veeco stated that they “recently experienced rescheduling of tool shipments from the fourth quarter into the first quarter by several customers in Korea and Taiwan.” In other words, pushouts! We will continue to see this more and more.

“Problem is, will the equipment vendors admit it? ASML vehemently denied any customers’ pushouts last quarter, but with tools selling for $35 million each and customers such as Nanya and Inotera announcing losses, there is no way in creation pushouts won’t happen.

“Then, there is the issue of 450mm wafers. The only ones pushing it are the semicons, because they recognized that they could generate twice the number of chips for almost the same capital equipment cost. The equipment industry was dramatically impacted by the 300mm transition, and growth was nearly flat from 2001 to 2009. Not so for the semicons.

“No equipment supplier wants 450mm, it is being pushed by Sematech and Intel, plus a consortium in Europe that feels that perhaps 450mm will knock off competitors and they can make up the vacuum in sales. Only the top 15 equipment suppliers will survive.”

How will pushouts benefit the industry?

On the subject of industry pushouts being highlighted time and again, it is also necessary to see whether and how will these benefit the industry in the long run.

Besides the reasons mentioned above, semiconductor sales are intimately tied to the economy. There is a direct correlation between semiconductor sales and GDP, as well as the PLIs of The Information Network. If the economy is robust, more money is available to purchase electronic items containing semiconductors. The reverse is true, indicative of the present economic climate.

The Information Network has also indicated that firms will announce lower results, and it’d get worse in the following quarter. Why will this happen and which firms could be likely ‘hurt’?

Dr. Castellano said: “This will happen because the crest in the tidal wave was only reached in the past month or so, and it is a long and slippery slope down because it went so high up to begin with.

“The DRAM manufacturers will be hit the hardest. Growth was strongest for them for the first half of the year, where sales grew 135 percent in Q2 2010 compared to Q2 2009.”

Is there a way out? If yes, when?

Finally, when will there be some recovery in the semiconductor equipment sales and why? Surely, as with everything, there has to be a way out!

Dr. Castellano concluded: “We see minimal growth in 2011, again depending on macroeconomic factors. We see two years of downturn in the industry – 2012 and 2013.”

Why has the semicon equipment bubble really burst? – I

Yesterday or early today, I’d mentioned about receiving an interesting report from The Information Network — where it said that the global semiconductor equipment industry bubble has burst!

It made interesting use of an analogy around “The Emperor’s New Clothes,” a short tale by Hans Christian Andersen and the global semiconductor industry. So, I got in touch with Dr. Robert N. Castellano, president of The Information Network, New Tripoli, USA, to find out more.

Just why did the bubble burst?

I started by asking him why The Information Network has been pointedly indicating that the semicon equipment bubble has burst?

He said: “If we take a look at the SEMI book-to-bill ratio, bookings were down from $1,837 million in July and $1,816 million in August to $1,616 million in September. Keep in mind that these are three-month moving averages. so that September’s numbers were proped up by stronger July and August bookings.

“Additional data come from our proprietary leading indicators (PLI) that we have developed obver the past 15 years. They point to changes and inflections in the economies of the world and correlate with inflections in semiconductor equipment revenues several months out. We plot SEMI’s announced billings (revenue) instead of bookings, which are anticipatory. Our PLI has been trending downward for the past three months, signalling an inflection in equipment revenues. We will see this happen this quarter.”

Pitfalls of two years of growth combined into one!

The report has also indicated that year 2010 is the same as 2000 — where two years of growth were combined into one. What are the pitfalls from such a development?

Dr. Castellano added that in 2000, equipment revenues skyrocketed, followed by a severe downturn in the following year. In a typical cycle, we see about three years of growth. But not so in 2000. The reason for the large growth was inaccurate market forecasts, when some ‘analysts’ kept hyping shortages in certain ICs, particularly DRAMs. This led IC manufacturers to purchase more equipment and build more fabs to meet the anticipated growth.

Little did they realize that the Dell Computers of the world were also reading the same ‘erroneous’ forecasts and purchasing twice the number of ICs they needed for fear of shortages.

The IC companies, not realizing the customers were double dipping, thought that the phenomenon was real and kept expanding. In 2001, IC manufacturers were left with about $10 billion in excess inventory. The year 2000 coincided with Y2K. Later that year, the Internet bubble also burst. So, growth came from anticipated applications, rather than real demand. Read more…

Global semicon industry update Mar. '10: Time for a reality check…pessimism has swung too far, says Future Horizons

The real significance of January is its potential impact on first quarter sales. Were this run rate to continue through February and March, first quarter sales would be up 8 percent versus Q4-09. That would make 2010 grow a staggering 40 percent on 2009. This is by no means a forecast but it does serve to illustrate the strength of the recovery from the abyss this time last year.

Ignoring the structurally (and typically) wild individual monthly fluctuations – which simply means no single month is a good indicator of the underlying trends – the month on month numbers will not settle down until the second quarter of 2010. That being said, given the likely strength of the first quarter versus Q4-09, our current 22 percent forecast for the total year now looks far too low.

Our 22 percent forecast for 2010 was based on the relatively benign quarterly growth pattern of -1.0, +1.0, +6.2 +2.0 percent; in essence a very weak year. No one we speak with is seeing a negative first quarter, with a consensus now building for at least 3 percent positive growth. That alone would bring the year on year growth up to 28 percent.

At the same time, almost everyone is also boasting a strong Q2 backlog with price stabilisation, even increasing; low inventory levels; and tightening supplies, which places severe doubt on the credibility of our plus 1 percent second quarter growth forecast. Were this to be say plus 3 percent, the year on year growth would be 30 percent.

It does however give us further confidence in our analysis and now places our forecast at the low end of the forecast range. Barring an epic 9/11, Act Of God or immoral banker style disaster, growth of anything less than 22 percent in 2010 is now all but impossible.

We fully expect to be increasing our forecast to around the plus 30 percent level at our forthcoming IEF2010 International Electronics Forum in Dresden, May 5-7 bringing the 2010 market within spitting distance of $300 billion in revenues. Read more…

Global semicon mid-year review: Chip market revival or blip on stats radar screen?

A recent report from Future Horizons suggests an 18 percent growth for the chip market in Q2-2009! So, is this a sign of the chip market recovery or a mere blip on the statistics radar screen?

It is both, said, Malcolm Penn, chairman, founder and CEO of Future Horizons, and counselled that: “The fourth quarter market collapse was far too steep — a severe over-reaction to last year’s gross financial uncertainty — culminating with the Lehman Brothers collapse in September. The first quarter saw this stabilise with the second quarter restocking, but there are other positive factors also in play.”

Examining a bit further, here’s what he further revealed. One, the memory market is seeing some signs of slow recovery. He said, “This has already started DDR3 driven!” Likewise, companies are also in the process of revising their forecasts. The reason, Penn contended, being, “The maths has changed dramatically since Jan 2009!”

According to him, factors now leading to conditions looking up in H2 2009, include the normal seasonal demand — from a tight inventory base — and tightening capacity. There is also a clear indication of the correction phase to rebalance over-depleted inventories having started. “This is what’s driving Q2’s high unit, and therefore, sales growth,” he contended.

Firms advised to stop seeing and waiting!

This isn’t all! Penn further counselled firms who are still in a wait-and-see mode to ‘stop seeing and waiting’! Next, fabs are also looking to maximize their returns. For one, they have stopped over-investing.

Do we have enough stats from others to back up what’s been happening in the global semiconductor industry? Perhaps, yes!

IC Insights stands out

First, look at IC Insights! It has stood out by pointing out in early July that H2-09 is likely to usher in strong seasonal strength for electronic system sales, a period of IC inventory replenishment, which began in 2Q09, and positive worldwide GDP growth.

IC Insights has predicted global IC market to grow +18 percent; IC foundry sales to grow +43 percent; and semiconductor capital spending to grow +28 percent in H2-09.

DDR3 driving memory recovery? Flat NAND?

Elsewhere, Converge Market Insights said that according to major DRAM manufacturers, DDR3 demand has been on the rise over the last two months and supply is limited.

This is quite in line with Future Horizons contention that there is a DDR3 driven memory recovery, albeit slow. It would be interesting to see how Q3-09 plays out.

As for NAND, according to DRAMeXchange, the NAND market may continue to show the tug-of-war status in July due to dissimilar positive and negative market factors perceived and expected by both sides. As a result, NAND Flash contract prices are likely to somewhat soften or stay flat in the short term.

Semicon equipment market to decline 52 percent in 2009!

According to SEMI, it projects 2009 semiconductor equipment sales to reach $14.14 billion as per the mid-year edition of the SEMI Capital Equipment Forecast, released by SEMI at the annual SEMICON West exposition.

The forecast indicates that, following a 31 percent market decline in 2008, the equipment market will decline another 52 percent in 2009, but will experience a rebound with annual growth of about 47 percent in 2010.

EDA cause for concern

The EDA industry still remains a cause for concern. The EDA Consortium’s Market Statistics Service (MSS) announced that the EDA industry revenue for Q1 2009 declined 10.7 percent to $1,192.1 million, compared to $1,334.2 million in Q1 2008, driven primarily by an accounting shift at one major EDA company. The four-quarter moving average declined 11.3 percent.

If you look at the last five quarters, the EDA industry has really been having it rough. Here are the numbers over the last five quarters, as per the Consortium:

* The EDA industry revenue for Q1 2008 declined 1.2 percent to $1,350.7 million compared to $1,366.8 million in Q1 2007.

* The industry revenue for Q2 2008 declined 3.7 percent to $1,357.4 million compared to $1,408.8 million in Q2 2007.

* The industry revenue for Q3 2008 declined 10.9 percent to $1,258.6 million compared to $1,412.1 million in Q3 2007.

* The industry revenue for Q4 2008 declined 17.7 percent to $1,318.7 million, compared to $1,602.7 million in Q4 2007.

Therefore, at the end of the day, what do you have? For now, the early recovery signs are more of a blip on the stats radar screen and there’s still some way to go and work to be done before the global semiconductor industry can clearly proclaim full recovery!

Before I close, a word about the Indian semiconductor industry. Perhaps, it needs to start moving a bit faster and quicker than it is doing presently. Borrowing a line from Malcolm Penn, the Indian semiconductor industry surely needs to “stop waiting and watching.”

I will be in conversation next with iSuppli on the chip and electronics industry forecasts. Keep watching this space, friends.

Reports of memory market recovery greatly exaggerated: iSuppli

EL SEGUNDO, USA: Concerned about their image as they face the specter of bankruptcy, many memory chip suppliers are attempting to paint a more optimistic picture of the business by talking up a potential market recovery.

However, while overall memory chip prices are expected to stabilize during the remaining quarters of 2009, iSuppli Corp. believes a true recovery in demand and profitability is not imminent.

After a 14.3 percent sequential decline in global revenue in the first quarter DRAM and NAND flash, the market for these products will grow throughout the rest of the year. Combined DRAM and NAND revenue will rise by 3.6 percent in the second quarter, and surge by 21.9 percent and 17.5 percent in the third and fourth quarters respectively.

“While this growth may spur some optimism among memory suppliers, the oversupply situation will continue to be acute,” said Nam Hyung Kim, director and chief analyst for memory ICs and storage at iSuppli.

“For example shipments of DRAM in the equivalent of the 1Gbit density will exceeded demand by an average of 14 percent during the first three quarters of 2009. This will prevent a strong price recovery, which will be required to achieve profitability for most memory suppliers.”

Painful oversupply

Due to a long-lasting glut of DRAM, the imbalance between supply and demand is too great for this market to recover to profitability any time soon.

“Even if all of the Taiwanese DRAM suppliers idled all their fabs, which equates to 25 percent of global DRAM megabit production, the market would remain in a state of oversupply,” Kim said. “This illustrates that the current oversupply is much more severe than many suppliers believe—or hope.”

Besides cutting capacity, which suppliers have already been doing, they presently have few options other than waiting for a fundamental demand recovery. iSuppli believes that another round of production cuts will take place in the second quarter, which will positively impact suppliers’ balance sheets late this year or early in 2010 at the earliest.

DRAM prices now amount to only one-third-level of Taiwanese suppliers’ cash costs. Unless prices increase by more than 200 percent, cash losses will persist for these Taiwanese suppliers.

While average megabit pricing for DRAM will rise during every quarter of 2009, it will not be even remotely enough to allow suppliers to generate profits in this industry. The industry needs a dramatic price recovery of a few hundred percentage points to make any kind of impact.

iSuppli is maintaining its “negative” rating of near-term market conditions for DRAM suppliers.

Confusing picture in NAND

The picture is a little more complicated in the NAND flash memory market.

Pricing for NAND since January has been better than iSuppli had expected. However, iSuppli believes this doesn’t signal a real market recovery.

Most NAND flash makers are continuing to lose money. The leading supplier, Samsung Electronics Co. Ltd., seems to be enjoying the current NAND price rally as prices have almost reached the company’s break-even costs. However, all the other NAND suppliers still are losing money.

“While the NAND market in the past has been able to achieve strong growth and solid pricing solely based on orders from Apple Computer Inc. for its popular iPod and iPhone products, this situation is not likely to recur in the future,” Kim said. “Even if Apple’s order surge, and it books most of Samsung’s capacity, it would require a commensurate increase in demand to other suppliers to generate a fundamental recovery in demand.”

However, iSuppli has not detected any substantial increase in orders from Apple to other suppliers. Furthermore, Apple’s orders, according to press reports, are not sufficient to positively impact the market as a whole.

It doesn’t make sense for major NAND suppliers Toshiba Corp. and Hynix Semiconductor Inc. to further decrease their production if there is a real fundamental market recovery. This means supply will continue to exceed demand and pricing will not rise enough to allow the NAND market as a whole to achieve profitability.

The NAND flash market is in a better situation than DRAM at least. However, the market remains challenging because fundamental demand conditions in the consumer electronics market have not improved due to the global recession.

One of the reasons why the price rally occurred is that inventory levels have been reduced in the channel and re-stocking activity has been progressing. Overall, memory suppliers will begin to announce their earnings shortly and iSuppli will remain cautious about the NAND flash market until we detect solid evidence, not just speculation, of a recovery.

iSuppli is remaining cautious about the near term rating of NAND market, holding its negative view for now, before considering upgrading it to neutral.

“Production cuts undoubtedly will have a positive impact on the market in the future. However, it’s too early for to celebrate. iSuppli believes the surge in optimism is premature. Supplier must be rational and watch the current market conditions carefully to avoid jumping to conclusions too quickly,” Kim concluded.

2009 DRAM CAPEX decreased by 56 percent: DRAMeXchange

The 2008 DRAM chip price dropped more than 85 percent, while the global DRAM industry has faced more than two years of cyclical downturn, and the consumer demand suddenly froze because of the global financial crisis in 2H08.

In 1Q09, the DDR2 667 MHz 1Gb chip price rebounded to an average of US$ 0.88, which fell between the material cost and cash cost level. Still, the DRAM vendors encountered huge cash outflow pressure. Not only were capacity cut conducted, the process migration schedules were also delayed in the wake of respective sharp CAPEX cuts.

In 1Q09, the DDR2 667 MHz 1Gb chip price rebounded to an average of US$ 0.88, which fell between the material cost and cash cost level. Still, the DRAM vendors encountered huge cash outflow pressure. Not only were capacity cut conducted, the process migration schedules were also delayed in the wake of respective sharp CAPEX cuts.

According to the survey of DRAMeXchange, the worldwide DRAM CAPEX of 2009 has been revised down to US$ 5.4 billion, sharply down by 56 percent, in contrast to the US$ 12.2 billion in 2008.

WW DRAM 50nm process migration schedules all deferred one to two quarters

From the roadmaps of DRAM vendors, the adoption schedule of DRAM mass production using the 50 nm process have now been delayed one to two quarters. DRAMeXchange estimates that by the end of 2009, the DDR3 will account for 30 percent of the standard DRAM.

Regarding the new DDR2 and DDR3 process migration, all DRAM vendors still own different types of strategies of density and types. For example, the Korean vendors’ 50 nm process migration schedules of DDR 3 are earlier than DDR2 and the 2 Gb DDR3 mass production schedule is earlier than the 1Gb chip.

As for the US and Japanese vendors, according to their DDR3 roadmap, the 50 nm process will be introduced between 3Q09 and 4Q09, which is later than the Korean vendors, and also firstly with mass production of 2 Gb DDR3. Therefore, in the DDR3 era, the density will mainly be 2 Gb which is a lower cost driver with more stimulating incentive to the market demand of higher density chips. The Taiwanese vendors are under the high cash pressure and are falling behind in the 50 nm process race. They are mainly focused on “pilot production”.

Gross die increases 40-50 percent as 50nm process drives down cost

According to the Moore’s Law, the number of transistors on an integrated circuit doubles every 12 months. After the process shrinking became more difficult in the recent decade, it increased to 24 months. With new process migration, the closer the line distance is the larger gross die number a single wafer gets, meanwhile the cost is lower and the vendors gain more competitiveness.

The average DRAM output increased about 30 percent during the process migration from 70nm to 60nm. With improvements of process design and die shrink in the same generation of process technology, the output can once again increase 20 percent. In the 50nm generation, the output will increase almost 40-50 percent, compared to 60nm process and the number of gross die increases to 1500-1700 per 12 inch wafer with another 30 percent cost down.

Cost of immersion lithography tools major capex of 50nm process migration

The major challenge of 50nm process migration is the lithography technology. The newest immersion lithography equipment is required and the older exposure equipment at the wavelength of 193nm is no longer suitable under 65nm process, due to physical limitations.

Traditional dry lithography uses air as the medium to image through masks. However, immersion lithography uses water as the medium. Immersion lithography puts water between the light source and wafer. The wavelength of light shrinks through water so it is able to project more precise and smaller images on the wafer. This is the invention that enabled the semiconductor process technology to migrate from 65nm to 45nm.

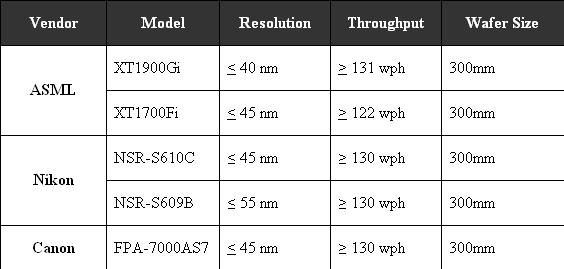

The current major immersion equipment vendors are ASML, Nikon, and Canon. The largest vendor in the market is AMSL, which is now mainly promoting its XT1900Gi, a tool that is capable to go lower than 40nm and is the most accepted model in the industry. Nikon still promotes its NSR-S610C, which was launched in 2007 and is able to go down to 45nm process. Canon launched its FPA-7000AS7 in mid 2008 that supports the process under 45nm.

No semicon recovery before mid 2010: Europartners

Connecting with new friends from all over the world is one of the best things that I have experienced while writing a semicon and electronics blog. One such gentleman is Ingo Guertler from Europartners Consultants. He is based in Munich, Germany — a city I have frequented several times.

Guertler has been part of my LinkedIn network as well. He has spent 30 years in leading positions in the electronic components market, mostly with semiconductors, at General Instrument, QT Optoelectronics and Vishay. Since 2005, he has been the senior partner at Europartners Consultants, a network of independent consultants, mostly located in Europe.

Beside individual projects, Europartners analyze the worldwide distribution market for electronic components each year and publish the results in its Worldwide Distribution Report.

Additionally, the company also organizes a two-day conference in Paris every two years, with high-level speakers out of the electronic component industry, discussing actual topics with top managers from component manufacturer and distributors.

This year, the headline will cover the world economy crisis, its effect on the electronics industry, and how companies can successful manage the crisis.

Naturally, our conversation revolved around the global semiconductor market, the memory market turmoil, and how European companies view the Indian semiconductor industry.

Semicon to decline 20 percent in 2009

Ingo Guertler expects a decrease in the global semiconductors market of approximately a minimum of 20 percent. Europartners does not see a recovery before the middle of 2010.

Guertler said: “Maybe, there can be a light recovery in the second quarter 2010 in some regions. Everything will depend on how fast the funds of the governments to the industry will draw. We have to specifically watch, the American and Chinese markets.”

Regarding the memory market, he added that everybody had expected that Vista will stimulate the markets. However, that did not happen. “For the time being, the industry has no direct killer application for memories available or in the design stage. I expect a further price erosion on memories, especially on DRAMs,” he cautioned.

Europe’s interest in Indian semicon

Again, it was natural for me to query Ingo on how European companies view the Indian semiconductor industry.

According to him, for the time being, collaboration between the European and Indian companies is limited in the most cases, or on a one-way service base, using the excellent skills and resources of the Indian software companies and engineers that also includes EDA. “I don’t think that will change in the near future,” he added.

Guertler said: “Personally, I see India as a new market challenge in the next 10 years or more for the European companies, because the local demand will grow faster in India, than we today see in China. Also, I believe and have seen it already, that a lot of companies will likely shift their production bases from China to India the next time, simply because of lower costs, availability of good, graduate engineers and a more Western orientated politics of the Indian government.”

However there is one handicap for the Indian continent! That is: the current infrastructure and the political situation between India and Pakistan.

According to Guertler, India has to set up huge investment programs to invite more investors in the country. Very importantly, is there any feeling that overseas companies’ interest in India is slowing down?

“Definitely not, as far as the European companies are concerned. If India meets the industry’s requirements, I believe their preference will be for India in comparison to China,” he said.

That indeed, is great to hear! The Indian interest is very much intact, in Europe and elsewhere. Now, it is time for India to get some work started on semiconductor product development companies.