Archive

Global semicon mid-year review: Chip market revival or blip on stats radar screen?

A recent report from Future Horizons suggests an 18 percent growth for the chip market in Q2-2009! So, is this a sign of the chip market recovery or a mere blip on the statistics radar screen?

It is both, said, Malcolm Penn, chairman, founder and CEO of Future Horizons, and counselled that: “The fourth quarter market collapse was far too steep — a severe over-reaction to last year’s gross financial uncertainty — culminating with the Lehman Brothers collapse in September. The first quarter saw this stabilise with the second quarter restocking, but there are other positive factors also in play.”

Examining a bit further, here’s what he further revealed. One, the memory market is seeing some signs of slow recovery. He said, “This has already started DDR3 driven!” Likewise, companies are also in the process of revising their forecasts. The reason, Penn contended, being, “The maths has changed dramatically since Jan 2009!”

According to him, factors now leading to conditions looking up in H2 2009, include the normal seasonal demand — from a tight inventory base — and tightening capacity. There is also a clear indication of the correction phase to rebalance over-depleted inventories having started. “This is what’s driving Q2’s high unit, and therefore, sales growth,” he contended.

Firms advised to stop seeing and waiting!

This isn’t all! Penn further counselled firms who are still in a wait-and-see mode to ‘stop seeing and waiting’! Next, fabs are also looking to maximize their returns. For one, they have stopped over-investing.

Do we have enough stats from others to back up what’s been happening in the global semiconductor industry? Perhaps, yes!

IC Insights stands out

First, look at IC Insights! It has stood out by pointing out in early July that H2-09 is likely to usher in strong seasonal strength for electronic system sales, a period of IC inventory replenishment, which began in 2Q09, and positive worldwide GDP growth.

IC Insights has predicted global IC market to grow +18 percent; IC foundry sales to grow +43 percent; and semiconductor capital spending to grow +28 percent in H2-09.

DDR3 driving memory recovery? Flat NAND?

Elsewhere, Converge Market Insights said that according to major DRAM manufacturers, DDR3 demand has been on the rise over the last two months and supply is limited.

This is quite in line with Future Horizons contention that there is a DDR3 driven memory recovery, albeit slow. It would be interesting to see how Q3-09 plays out.

As for NAND, according to DRAMeXchange, the NAND market may continue to show the tug-of-war status in July due to dissimilar positive and negative market factors perceived and expected by both sides. As a result, NAND Flash contract prices are likely to somewhat soften or stay flat in the short term.

Semicon equipment market to decline 52 percent in 2009!

According to SEMI, it projects 2009 semiconductor equipment sales to reach $14.14 billion as per the mid-year edition of the SEMI Capital Equipment Forecast, released by SEMI at the annual SEMICON West exposition.

The forecast indicates that, following a 31 percent market decline in 2008, the equipment market will decline another 52 percent in 2009, but will experience a rebound with annual growth of about 47 percent in 2010.

EDA cause for concern

The EDA industry still remains a cause for concern. The EDA Consortium’s Market Statistics Service (MSS) announced that the EDA industry revenue for Q1 2009 declined 10.7 percent to $1,192.1 million, compared to $1,334.2 million in Q1 2008, driven primarily by an accounting shift at one major EDA company. The four-quarter moving average declined 11.3 percent.

If you look at the last five quarters, the EDA industry has really been having it rough. Here are the numbers over the last five quarters, as per the Consortium:

* The EDA industry revenue for Q1 2008 declined 1.2 percent to $1,350.7 million compared to $1,366.8 million in Q1 2007.

* The industry revenue for Q2 2008 declined 3.7 percent to $1,357.4 million compared to $1,408.8 million in Q2 2007.

* The industry revenue for Q3 2008 declined 10.9 percent to $1,258.6 million compared to $1,412.1 million in Q3 2007.

* The industry revenue for Q4 2008 declined 17.7 percent to $1,318.7 million, compared to $1,602.7 million in Q4 2007.

Therefore, at the end of the day, what do you have? For now, the early recovery signs are more of a blip on the stats radar screen and there’s still some way to go and work to be done before the global semiconductor industry can clearly proclaim full recovery!

Before I close, a word about the Indian semiconductor industry. Perhaps, it needs to start moving a bit faster and quicker than it is doing presently. Borrowing a line from Malcolm Penn, the Indian semiconductor industry surely needs to “stop waiting and watching.”

I will be in conversation next with iSuppli on the chip and electronics industry forecasts. Keep watching this space, friends.

2009 DRAM CAPEX decreased by 56 percent: DRAMeXchange

The 2008 DRAM chip price dropped more than 85 percent, while the global DRAM industry has faced more than two years of cyclical downturn, and the consumer demand suddenly froze because of the global financial crisis in 2H08.

In 1Q09, the DDR2 667 MHz 1Gb chip price rebounded to an average of US$ 0.88, which fell between the material cost and cash cost level. Still, the DRAM vendors encountered huge cash outflow pressure. Not only were capacity cut conducted, the process migration schedules were also delayed in the wake of respective sharp CAPEX cuts.

In 1Q09, the DDR2 667 MHz 1Gb chip price rebounded to an average of US$ 0.88, which fell between the material cost and cash cost level. Still, the DRAM vendors encountered huge cash outflow pressure. Not only were capacity cut conducted, the process migration schedules were also delayed in the wake of respective sharp CAPEX cuts.

According to the survey of DRAMeXchange, the worldwide DRAM CAPEX of 2009 has been revised down to US$ 5.4 billion, sharply down by 56 percent, in contrast to the US$ 12.2 billion in 2008.

WW DRAM 50nm process migration schedules all deferred one to two quarters

From the roadmaps of DRAM vendors, the adoption schedule of DRAM mass production using the 50 nm process have now been delayed one to two quarters. DRAMeXchange estimates that by the end of 2009, the DDR3 will account for 30 percent of the standard DRAM.

Regarding the new DDR2 and DDR3 process migration, all DRAM vendors still own different types of strategies of density and types. For example, the Korean vendors’ 50 nm process migration schedules of DDR 3 are earlier than DDR2 and the 2 Gb DDR3 mass production schedule is earlier than the 1Gb chip.

As for the US and Japanese vendors, according to their DDR3 roadmap, the 50 nm process will be introduced between 3Q09 and 4Q09, which is later than the Korean vendors, and also firstly with mass production of 2 Gb DDR3. Therefore, in the DDR3 era, the density will mainly be 2 Gb which is a lower cost driver with more stimulating incentive to the market demand of higher density chips. The Taiwanese vendors are under the high cash pressure and are falling behind in the 50 nm process race. They are mainly focused on “pilot production”.

Gross die increases 40-50 percent as 50nm process drives down cost

According to the Moore’s Law, the number of transistors on an integrated circuit doubles every 12 months. After the process shrinking became more difficult in the recent decade, it increased to 24 months. With new process migration, the closer the line distance is the larger gross die number a single wafer gets, meanwhile the cost is lower and the vendors gain more competitiveness.

The average DRAM output increased about 30 percent during the process migration from 70nm to 60nm. With improvements of process design and die shrink in the same generation of process technology, the output can once again increase 20 percent. In the 50nm generation, the output will increase almost 40-50 percent, compared to 60nm process and the number of gross die increases to 1500-1700 per 12 inch wafer with another 30 percent cost down.

Cost of immersion lithography tools major capex of 50nm process migration

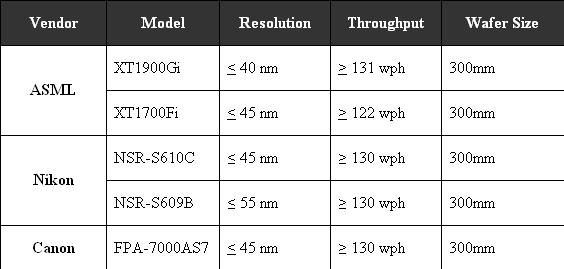

The major challenge of 50nm process migration is the lithography technology. The newest immersion lithography equipment is required and the older exposure equipment at the wavelength of 193nm is no longer suitable under 65nm process, due to physical limitations.

Traditional dry lithography uses air as the medium to image through masks. However, immersion lithography uses water as the medium. Immersion lithography puts water between the light source and wafer. The wavelength of light shrinks through water so it is able to project more precise and smaller images on the wafer. This is the invention that enabled the semiconductor process technology to migrate from 65nm to 45nm.

The current major immersion equipment vendors are ASML, Nikon, and Canon. The largest vendor in the market is AMSL, which is now mainly promoting its XT1900Gi, a tool that is capable to go lower than 40nm and is the most accepted model in the industry. Nikon still promotes its NSR-S610C, which was launched in 2007 and is able to go down to 45nm process. Canon launched its FPA-7000AS7 in mid 2008 that supports the process under 45nm.

Top NAND suppliers of the world: DRAMeXchange

DRAMeXchange has recently released its rankings for the top NAND suppliers of the world. I am producing bits of that report here, for the benefit of those interested in NAND and the memory market.

Be aware, that this segment has been hit particularly bad. We have heard of Qimonda’s problems, as well as Spansion’s. They are trying to battle it out, gamefully, and best wishes to them.

The global semiconductor industry needs the flash memory segment to recover, and fast, to bring the health back in the industry, as well as the missing buzz!

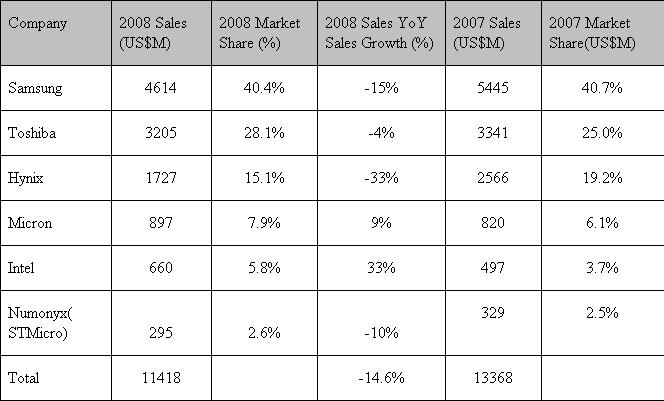

Getting back to DRAMeXchange’s report, NAND Flash brand companies released their total revenue of 2008. Samsung’s annual revenue was $4.614 billion and it gained 40.4 percent market share, to maintain the number 1. position.

According to DRAMeXchange, the annual revenue of Toshiba was $3.25 billion, and its market share was 28.1 percent at the number 2 position. Its market share increased 3.1 percent compared to 2007.

According to DRAMeXchange, the annual revenue of Toshiba was $3.25 billion, and its market share was 28.1 percent at the number 2 position. Its market share increased 3.1 percent compared to 2007.

Hynix’s annual revenue was $1.727 billion, with 15.1 percent market share. Though it stayed at the number 3 position, its market share declined 4.1 percent, compared to 2007.

Micron’s annual revenue was $897 million. It had a 7.9 percent market share, which enjoyed a 1.8 percent increase when compared to 2007. Micron was number 4. Intel was at number 5. Its annual revenue was $660 million with 5.8 percent market share, which increased 2.1 percent, compared to 2007.

Numonyx’s (STMicro) 2008 annual revenue was $295 million. It was at number 6 position with the market share of 2.6 percent, which remained the same as 2007.

According to DRAMeXchange, the 4Q08 total revenue of worldwide NAND Flash brand companies was $2.227 billion, which dropped 19.3 percent from $2.761 billion in 3Q08. Under the continuing impact of global recession and the influence of declining worldwide consumer confidence, the 4Q08 revenue of NAND Flash brand companies showed signs of decreasing.

The overall demand and expenditure for consumer electronics declined. Although bit growth in 4Q08 increased 18 percent QoQ, the overall average selling price (ASP) dropped 32 percent QoQ, says DRAMeXchange. A big thanks to DRAMeXchange.

DRAM makers being offered lifelines via bail out plans!

Browsing the Web these past days has brought me to various stories, mostly discussing the various bail out plans being provided for some leading DRAM makers.

It all started with Germany based Qimonda announcing that it has arranged a Euro 325 million financing package for the ramp up of its innovative Buried Wordline technology.

Yesterday, Hynix, the Korean DRAM maker, received a bail out of $597 million, according to reports on Fabtech. The story also reports that Powerchip Semiconductor, Taiwan’s largest DRAM maker, is also seeking new funding.

Then, DigiTimes, a very good technology news Web site from Taiwan, reported yesterday that Taiwan’s Ministry of Economic Affairs (MoEA) had reportedly developed an NT$200 billion (US $6.5 billion) bail out plan for Taiwan’s hard-hit DRAM makers.

Sitting in India makes it a little difficult to speak with global companies based in Taiwan, Korea and Germany. I sometimes wish I could get some help from reliable sources as to what’s the actual ground situation.

Having said that, it is good to see various national governments showing their deep concern about the state of the global DRAM industry and about technologies. And, let us keep all criticisms aside, as to who performed and who didn’t! Here’s a lesson for India to learn from, as closer home, it has a semiconductor industry really in its infancy!

Right now, the global semiconductor industry is facing a downturn and memory is the hardest hit! Hence, if any measures are being taken to somehow bring DRAM back on track, it should be welcomed.

Qimonda, Hynix, Powerchip, etc., are not small names in the global industry. Poor performance from memory players saw them dropping out of the top 20 global semiconductor players’ rankings in 2008.

All the lifelines being provided to these major players now means that these companies need to pull it off, somehow, and extricate themselves from the depths they have fallen into. If they fail, they will perish! And, they all know that!!

I’d be very keen to see the responses of DRAMeXchange and iSuppli on these bail out plans.

Merry X’mas everyone, and hope you all have a great time!

PS: I have iSuppli’s feedback!

Speaking on the Taiwan government’s bail-out plan as well as Hynix’s rescue package from banks, John Lei, Analyst, memory, iSuppli Corp., said: “In general, Hynix’s package is much like a short-term relief for their near-term debt, while the Taiwan government aims at the possible consolidation of five suppliers.”

“All these packages could bring more uncertainties to the maket, however, based on iSuppli’s assumption and forecasts. The industry operation profit margin will hit bottom in Q4-08, but profitability of the industry will not occur until Q4-09,” he added.

How Taiwan government reacts to DRAM turmoil is a lesson in itself!

Taiwan based DRAMeXchange recently sent me a release, which discussed in length the steps the Taiwan government is taking in an attempt to “save one of the ‘2 trillion twin stars’, the DRAM industry”. The Taiwanese Ministry of Economic Affairs (MoEA) was designated to draft the policies, principals, strategic goals and strategic directions of the DRAM industry rescue plan.

According to DRAMeXchange: At 6 PM, December 16, the Taiwanese Ministry of Economic Affairs held a press conference about the DRAM rescue plan, emphasized in the past 10 years the investment amount of the DRAM industry surpassed NT$ 850 billion, and created a complete industry supply chain, which widely covers upstream chip makers, to downstream packaging and testing companies, and module houses. If the recession brought down the industry, the Taiwan industrial chain will be affected severely.

The Taiwanese government showed sincerity and willingness, and hoped that Taiwanese DRAM vendors can actively start to consolidate horizontally and vertically, and make joint proposing plans to the government. The government will not take the leading position, but the strategic direction is long term integration, which is not just merger but also includes cooperation of co-research, co-develop, and co-manufacturing.

The government also emphasized that it will tend to strengthen the relationship among the co-operation of Taiwanese, American, and Japanese DRAM vendors.

In another report, Gartner has gone as far as dubbing the DRAM industry as the wild card for the semiconductor industry in 2009! The DRAM industry has been in a downturn for the past 18 months and losses are now approaching $12 billion, it says.

How the Taiwanese DRAM industry reacts to the efforts of the Taiwan government will be visible in the coming months. Among other bail out plans, the Taiwan government has also focused on the need for the local industry to develop its own technology.

Taiwan takes great pride in having been a leader in technology and R&D for long. If the DRAM industry does not recover quickly enough, it would indeed impact the country’s industrial chain as well.

What’s interesting to note is the key role the government of Taiwan is playing in all of this. It again stresses the importance of government contribution within the semiconductor industry. And, there is also a lesson in all of this for India!

Closer home, in India, I am (and I am sure, interested readers and parties are too) still waiting to hear on what happened to the several proposals that were received for solar/PV, as well as on the various state policies, especially, Karnataka.

All believe that these would surely get pushed through in the new year. However, there is a need to show some speed in this regard as well. You cannot afford to wait for too long in the semiconductor industry. The SemIndia fab story is all to well known and hopefully, still fresh in everyone’s minds.

Semicon to grow 4-8pc in 2008; ASPs trending up

It has really been a tumultuous year for semiconductors, which has held up very well, despite the memory market turmoils, so far.

Just a day ago, Future Horizons reported on the June sales for semiconductors. According to Malcolm Penn, chairman and CEO, June’s WSTS results brought both good and bad news! The good news being that the recovery momentum strengthened, with Q2 sales up 3 percent on Q1.

Just a day ago, Future Horizons reported on the June sales for semiconductors. According to Malcolm Penn, chairman and CEO, June’s WSTS results brought both good and bad news! The good news being that the recovery momentum strengthened, with Q2 sales up 3 percent on Q1.

He says, “This was significantly better than even we dared to predict in last month’s Report, despite the fact we raised eyebrows and disbelief by suggesting a 2.3 percent quarter on quarter growth.”

The bad news was the Jan-May YTD WSTS numbers for standard logic (and thus, the total ICs and total SC) were revised downwards by a sizeable US$1.4 billion, a restatement that will knock 2 percentage points off the 2008 year on year growth number!

What were the reasons for the recovery momentum to have strengthened, with Q2 sales up 3 percent on Q1? Penn adds: “The first half year sales were much stronger than everyone (except us) believed. It has depresses, only by memories.”

Also, the Jan-May YTD WSTS numbers for standard logic (and total ICs and total SC) were revised downward by a sizeable US$1.4 billion. Why did this happen? It is interesting to note that one company mis-reported its sales for Jan-May and corrected this reporting error in June.

Penn adds: “This often happens, but not before at this magnitude. Individual company details are secret, so we do not know who the culprit was or how the ‘error’ happened.”

Forecast revised to 4-8 percent

Future Horizons further says in its report that the downward revision in standard logic numbers would knock 2 percentage points off the 2008 year on year growth number. On quizzing, Penn agrees: “Yes, our ‘revised’ forecast range is 4-8 percent. We are currently still erring on the high side of this range. More important though is the market momentum.”

Memory has been a constant problem this year. iSuppli has mentioned in an earlier report that NAND recovery will be likely in H2-2009.

DRAMeXchange, in another report today, indicates a new record low for DDR 1Gb. Even Penn agrees that recovery is definitely not in sight. When do we actually get to see some recovery? He adds: “There is still over capacity, however, Q3 is typically the strongest demand quarter.”

Still on memory, does Future Horizons forsee Hynix bouncing back? Penn says: “They did; in 2000-02, they were on the verge of bankruptcy. Now, they are fitter and financially strong.”

ASPs were trending up earlier, and the status quo is maintained. “ASPs are still trending up, slowly, but surely. We will be commenting more on this in September’s report,” he adds.

Fab spends trending down

Just a few days ago, a SEMI analyst highlighted the chief reasons for decline in fab spends. Christian Gregor Dieseldorff, Senior Manager of Fab Information and Analysis at SEMI, said: “Given the weaker economic conditions globally, coupled with higher energy and commodity prices and the financial crisis, the overall outlook for semiconductor growth in 2008 is for low-single digit growth in both revenues and units. As such, device makers have responded by cutting back their capital spending and pushing out fab projects or putting them on hold.”

On the status with fab spends, Penn agrees, “Those are still trending down, and will continue to do so for at least the next three quarters.”

Solar not much help

There have been lot of investments happening in solar/PV. One may imagine that all of this would be helping the global semiconductor industry. So, is the spend in solar/PV really helping the industry? Penn disagrees, saying this only helps the equipment guys.

One last query, and this is regarding the smaller IDMs, ‘fab-lite’ IDMs, and fabless semiconductor companies. Are they growing at below average? Penn concludes: “They are mostly not. The fabless firms outgrew the market 2x in the first half of 2008.”

Perhaps, here also lies a message for India!! One hopes that India does not get too carried away by all those investments in solar/PV, and focuses more on the semicon side. Semicon in India, does need concrete planning, after all!

Semicon is no longer business as usual!

The Global Semiconductor Monthly Report June 2008 from Future Horizons, states: Let the market beware; it is no longer business as usual!

I would completely agree! For instance, the industry has since long moved to fabless, and now, fabless firms are ranking among the very best. Or, even from 130nm to 22nm process nodes, or from 180mm fabs to 450mm fabs!! Fair enough?

Coming back to the industry trends, Malcom Penn, CEO, Future Horizons, says that compared with March, the IC units were up and ASPs were down in April, even after adjusting for March being a five-week month. The net result was a 7.7 percent revenue decline! Does this spell more bad news for the beleaguered chip market?

Certainly, this seems to be the industry consensus view. Always the contrarian, Future Horizons’ views are different. Here’s how! April’s results came in exactly as expected. Also, the unit rise and fall was simply the result of the engrained ‘making the quarterly number’ mentality!

Digging beneath the layers reveals a set of market fundamentals that are in remarkably strong form. The penny may not yet have dropped to the table, but, even for the chip industry ever full of surprises, let the market beware; it is no longer business as usual.

Penn says: To paraphrase the late Sir Winston Churchill’s comments on Russia, “The chip industry too is a riddle wrapped up in an enigma”. It marches to its own complex interwoven pattern of rules, each relatively simple when viewed in isolation, but contriving to interact in a volatile and unique way. Right now, the industry is at its most confused [state] for a decade, battered by a barrage of uncertainties and contradictions. Shell-shocked and confused, confidence is off the agenda … just when what is needed most is cool heads and determination.”

Be it falling cap ex, tight capacity, focus on profits, continuing strong market demand, second half seasonal effects, according to him, the forecast tea leaves all seem to be pointing in the same positive direction. Has the worm finally turned then for the industry? He thinks so! Future Horizons also thinks that the “penny has yet to drop and that the impact on the market will be seismic and dramatic”.

Earlier, the Semiconductor Industry Association (SIA) reported that worldwide sales of semiconductors of $21.8 billion in May were 7.5 percent higher than the $20.3 billion reported for May 2007, reflecting continued strong sales of consumer electronic products. May sales were 2.8 percent higher than the $21.2 billion reported for April 2008.

Do bear in mind that May is historically a strong month for semiconductor sales, as per SIA.

NAND strong minus Apple effect

DRAMeXchange has indicated in its monthly review on the DRAM segment that the NAND Flash prices are likely to gradually stabilize after mid-July pushing by lower price, new demand from 3G iPhone, smart phones and low-cost PCs.

Elsewhere, as reported by Semiconductor International, according to Semico, NAND unit shipments are likely to cross over 3.5 billion units in 2008 as against 2.5 billion units in 2007, leading to a year-over-year growth of 35 percent.

However, reflecting the memory segment’s ASP (average selling price) crunch, NAND revenues will grow 13 percent in 2008, down compared to 25 percent in 2007.” Semico has said that the NAND industry will record a growth year in 2008, without experiencing what it has called the ‘Apple effect’.

Heartening solar initiatives

The one heartening thing to note has been the various solar related initiatives that have taken place over the past month (actually, for over the year!). In fact, iSuppli has probably been spot on while analyzing that investments in solar and semiconductors could be on par by 2010!

SVTC Technologies, an independent semiconductor process-development foundry, announced that its SVTC Solar business unit has launched the Silicon Valley Photovoltaic Development Center in San Jose. Canadian Solar and LDK Solar signing a new agreement for an additional 800MW of solar wafers, besides LDK updating on its polysilicon plant in China.

National Semiconductors also entered the PV market with its SolarMagic technology that maximizes solar energy production. Evergreen Solar, a maker of solar power panels with its proprietary, low-cost String Ribbon wafer technology, signed two new long-term sales contracts. Tokyo Ohka Kogyo Co. Ltd and IBM are also collaborating to establish new, low-cost methods for developing the next generation of solar energy products.

Not be left behind, Intel too is spinning off key assets of a start-up business effort inside Intel’s New Business Initiatives group to form an independent firm called SpectraWatt.

In India, solar has been making rapid strides, especially at the Fab City in Hyderabad. There is a possibility of something similar happening in Karnataka state as well.

Indeed, semiconductors are no longer business as usual! Right?

Top 20 global semicon companies — DRAM, Flash suppliers drop out

IC Insights recently published the May update to The McClean Report, featuring the Top 20 global semiconductor companies. Not surprisingly, there have been some significant movers and shakers. The most telling — quite a few of the major DRAM and Flash suppliers have dropped out of the Top 20 list!

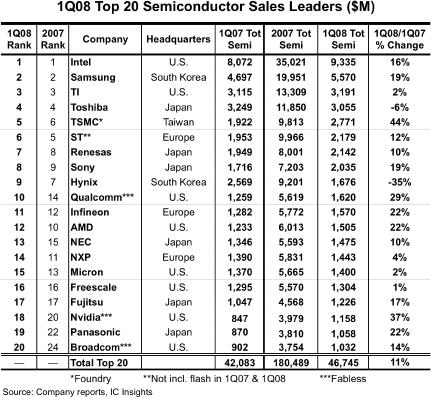

First the movers! Fabless supplier Qualcomm jumped up four spots, ranking as the 10th largest semiconductor supplier in Q1-08. Next, Broadcom, the third largest fabless supplier, also moved up four positions, up to the 20th position. Panasonic (earlier, Matsushita), moved up to the 19th position, while NEC of Japan moved up to the 13th position.

First the movers! Fabless supplier Qualcomm jumped up four spots, ranking as the 10th largest semiconductor supplier in Q1-08. Next, Broadcom, the third largest fabless supplier, also moved up four positions, up to the 20th position. Panasonic (earlier, Matsushita), moved up to the 19th position, while NEC of Japan moved up to the 13th position.

TSMC, the leading foundry, moved up one position, registering the highest — 44 percent — year-over-year Q1-08 growth rate, besides being ranked 5th. Nvidia, the second largest fabless supplier, was another company registering a high YoY growth rate of 37 percent, and moved into the 18th position. Some others like Infineon, Sony and Renesas also climbed a place higher each, respectively. The top four retained their positions — Intel, Samsung, TI and Toshiba.

And now, the shakers! The volatile DRAM and Flash markets have ensured the exit of several well known names such as Qimonda, Elpida, Spansion, Powerchip, Nanya, etc., from the list of the top 20 global semiconductor companies, at least for now.

Among the others in the list, the biggest drops were registered by NXP, which dropped to 14th from 11th last year, and AMD, which dropped two places, from 10th to 12th. Two memory suppliers — Hynix and Micron — also slipped two places, to 9th and 15th places, respectively. STMicroelectronics also slipped from 5th to 6th. IBM too slipped out of the top 20 list.

The top 20 global semiconductor firms comprises of eight US companies (including three fabless suppliers), six Japanese, three European, two South Korean, and one Taiwanese foundry (TSMC). Also, looking at the realities of the foundry market, TSMC’s lead is now unassailable. If TSMC was an IDM, it would be No. 2, challenging Intel and passing Samsung, said one analyst, recently, a thought shared by many.

IC Insights has reported that since the Euro and the Yen are strong against the dollar, this effect will impact global semiconductor market figures when reported in US dollars this year.

There are some other things to watch out for. Following a miserable 2007, the global DRAM module market is likely to rebound gradually in 2008 due to the projected recovery in the overall memory industry, according to an iSuppli report. That remains to be seen.

Some new DRAM camps — such as Elpida-Qimonda, and Micron-Nanya — have been formed. It will be interesting to see how these perform, as will be the performance of ST-backed Numonyx.

Further, the oversupply of NAND Flash worsened in Q1-08, impacted by the effect of the US sub-prime mortgage loan and a slow season, according to DRAMeXchange. The NAND Flash ASP fell about 35 percent compared to Q4-07. Although the overall bit shipment grew about 30 percent compared to Q4-07, the total Q1-08 sales of branded NAND Flash makers fell 15.8 percent QoQ to US$3.24bn. Will the NAND Flash market recover and by when?

New camps promise exciting times ahead in memory market

The last few weeks of this month witnessed some interesting developments in DRAM. No, there are not signs of a recovery, yet. Instead, the appearance of new DRAM camps, as well as a new memory interface working group, does generate some interest.

However, first, the stats. DRAMeXchange recently reported that the Q1-08 revenues of the branded DRAM makers, impacted by continual low DRAM prices, fell by roughly 5.8 percent compared to Q4-07. Likewise, the contract prices and the spot prices fell 19 percent and 11 percent respectively.

DRAMeXchange further reported that barring Elpida and Powerchip, all other DRAM makers experienced a decline in revenues. Both Elpida and Powerchip witnessed slight increase in their market share during Q1-08.

Categorizing the DRAM industry market share by countries, Japan only increased by 0.9 percent from 13.5 percent to 14.4 percent, as Elpida’s revenue increased in Q108. Taiwan’s share increased by only 1.1 percent from 13.6 percent to 14.7 percent, as Powerchip gained market share. Korea sustained the same market shares — 47.2 percent, as in Q4-07.

However, America and Germany lost share. America’s share slipped from 13.6 percent to 13 percent, while Germany’s share fell from 12.2 percent to 10.8 percent, respectively.

In a recent investor conference, Samsung announced it will increase its Bit Growth Rate from 70 percent to 100 percent, an indication of its desire to continue reigning as a DRAM market leader.

Now, to the really interesting developments. First, Nanya and Micron signed an agreement to create MeiYa Technology Corp., a new DRAM joint venture. One of Nanya’s 200mm facility in Taiwan will be upgraded to 300mm starting this year, with the facility going online for production in 2009. Besides MeiYa, Nanya and Micron will co-develop and share future technology.

If this wasn’t enough, close on the heels of the Micron-Nanya JV, Elpida Memory and Qimonda AG, signed a Memorandum of Understanding (MoU) for a technology partnership for jointly developing memory chips (DRAMs), and accelerate their roadmap to DRAM products featuring cell sizes of 4F2.

Analysts at DRAMeXchange believe that the Qimonda-Elpida alliance re-shuffles the DRAM competitive landscape. It is also a sign of Qimonda’s determination to develop stacked process.

Lastly, ARM, Hynix Semiconductor Inc., LG Electronics, Samsung Electronics, Silicon Image Inc., Sony Ericsson Mobile Communications AB, and STMicroelectronics announced the formation of a working group, the Serial Port Memory Technology (SPMT), which is committed to creating an open standard for next-generation memory interface technology targeting mobile devices.

SPMT, a first-of-its-kind memory standard for DRAM, is said to enable an extended battery life, bandwidth flexibility, significantly reduced pin count, lower power demand and multiple ports by using a serial interface instead of a parallel interface commonly used in today’s memory devices.

Handset vendors have joined the fray as this technology will not only extend battery life, it will allow high-performance media-rich applications as well, that are likely to be the norm on next-generation mobile phones.

Surely, these developments and the emergence of new camps promise some exciting times ahead in the memory market.