Archive

Top NAND suppliers of the world: DRAMeXchange

DRAMeXchange has recently released its rankings for the top NAND suppliers of the world. I am producing bits of that report here, for the benefit of those interested in NAND and the memory market.

Be aware, that this segment has been hit particularly bad. We have heard of Qimonda’s problems, as well as Spansion’s. They are trying to battle it out, gamefully, and best wishes to them.

The global semiconductor industry needs the flash memory segment to recover, and fast, to bring the health back in the industry, as well as the missing buzz!

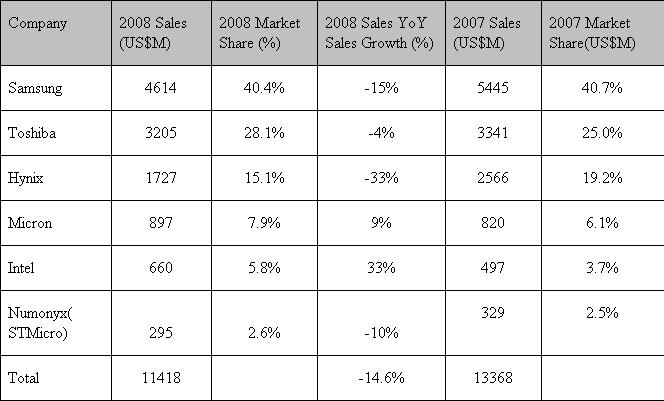

Getting back to DRAMeXchange’s report, NAND Flash brand companies released their total revenue of 2008. Samsung’s annual revenue was $4.614 billion and it gained 40.4 percent market share, to maintain the number 1. position.

According to DRAMeXchange, the annual revenue of Toshiba was $3.25 billion, and its market share was 28.1 percent at the number 2 position. Its market share increased 3.1 percent compared to 2007.

According to DRAMeXchange, the annual revenue of Toshiba was $3.25 billion, and its market share was 28.1 percent at the number 2 position. Its market share increased 3.1 percent compared to 2007.

Hynix’s annual revenue was $1.727 billion, with 15.1 percent market share. Though it stayed at the number 3 position, its market share declined 4.1 percent, compared to 2007.

Micron’s annual revenue was $897 million. It had a 7.9 percent market share, which enjoyed a 1.8 percent increase when compared to 2007. Micron was number 4. Intel was at number 5. Its annual revenue was $660 million with 5.8 percent market share, which increased 2.1 percent, compared to 2007.

Numonyx’s (STMicro) 2008 annual revenue was $295 million. It was at number 6 position with the market share of 2.6 percent, which remained the same as 2007.

According to DRAMeXchange, the 4Q08 total revenue of worldwide NAND Flash brand companies was $2.227 billion, which dropped 19.3 percent from $2.761 billion in 3Q08. Under the continuing impact of global recession and the influence of declining worldwide consumer confidence, the 4Q08 revenue of NAND Flash brand companies showed signs of decreasing.

The overall demand and expenditure for consumer electronics declined. Although bit growth in 4Q08 increased 18 percent QoQ, the overall average selling price (ASP) dropped 32 percent QoQ, says DRAMeXchange. A big thanks to DRAMeXchange.

NAND update: Market likely to recover in H2-09

iSuppli’s recently published a report on the current NAND market conditions, which highlighted that Micron had managed to buck the weak NAND market conditions, and was actually closing the gap with Hynix in Q2 2008.

To find out more about the global NAND Flash market scenario, I managed to discuss the health of the NAND market conditions, performance of certain companies, and the possible impact of SSDs on the NAND market, in depth with Nam Hyung Kim, Director & Chief Analyst, Memory, for the market research firm, iSuppli Corp., El Segundo, Calif., USA.

To find out more about the global NAND Flash market scenario, I managed to discuss the health of the NAND market conditions, performance of certain companies, and the possible impact of SSDs on the NAND market, in depth with Nam Hyung Kim, Director & Chief Analyst, Memory, for the market research firm, iSuppli Corp., El Segundo, Calif., USA.

I would also like to thank Jonathan Cassell, Editorial Director and Manager, Public Relations, iSuppli, for helping me out a lot! Without his assistance, this would not have been possible! Many thanks.

Now on to iSuppli and the NAND update. First up, NAND continues to be weak. How much longer, before we can see some sort of recovery?

Nam Hyung Kim says that the NAND market conditions will depend on the suppliers’ manufacturing capacity plans and on the global economy. The health of the NAND flash market is largely determined by consumer spending, since more than 85 percent of demand for the memory is generated by consumer-electronics-type products like digital still cameras, mobile handsets and flash storage devices.

“Market conditions won’t improve much this quarter. However, iSuppli Corp. does expect NAND prices to stabilize to some degree during the fourth quarter due to a slowdown in certain suppliers’ capacity expansion plans. A major recovery is expected in the second half of 2009,” he says.

So, what’s the reason for Micron to have done better in a weak market scenario?

According to Kim, Micron is doing well based on market share and sales growth—but not in terms of profitability. Micron has been expanding its market share by ramping up production aggressively. The company joined the flash market later than its competitors and is trying to catch up. In the memory world, a supplier needs to have critical scale. Without scale, the company won’t be competitive. Thus, Micron is increasing its scale—i.e., its volume—to be more like the size of the top-three suppliers at this moment.

If Micron has been aggressive, why haven’t the others? Possibly, the others could have also planned or migrate to 34nm! However, except for Samsung, all of the suppliers are losing money in their NAND businesses now.

“Each supplier has a different product mix and strategy, so being aggressive during tough times is not a suitable approach for certain firms. Others also plan to migrate their process to sub 40 nanometers. However, Micron will be the first one that produces 34nm products this year,” adds Kim.

iSuppli has now cut its 2008 NAND annual flash revenue growth forecast from 9 percent to virtually zero. When the slowdown had already been predicted during the end of last year, what was the need to cut predictions?

Kim agrees that this is indeed the second cut this year. “We cut our forecast early this year to 9 percent, which was a dramatic reduction from the more than 20 percent growth forecast previously. I believe, we were the first research firm that cut the market growth dramatically this year, followed by other research firms.

“The NAND flash market is relatively new and has lots of growth potential. However, oversupply issues, along with weak consumer spending, prompted us to cut the growth outlook further this time.”

Coming to the subject of solid-state drives, what are the chances of SSDs in helping with a turnaround in the NAND market? Or, are they (SSDs) hyped?

“I should not say SSDs (solid-state drives) are overhyped,” adds Kim. “There are lots of issues that the industry must overcome when bringing SSD technology to the real world. Hard disk drives (HDDs) have been used in PCs for more than 30 years, so the movement to SSD technology won’t be very rapid.”

iSuppli had predicted that SSDs would not impact the market this year or next year. The real prime time for SSD adoption will be in 2010. There are many optimization problems associated with SSDs, which is typical at an early stage in the technology industry. By 2011, iSuppli believes SSDs will be the number one NAND flash market driver in terms of dollar value.

iSuppli also believes that the global NAND flash per-megabit average selling price (ASP) will decline by about 60 percent in 2008, compared to its previous forecast of a 56 percent decline. On quizzing, he says, “As mentioned, the NAND flash market, even in third-quarter, holiday season, won’t have a turn around, which brings the ASP down to the 60 percent level.”

When NAND is taken out of the equation, how does the semiconductor industry look like? iSuppli believes that the 2009 global semiconductor market growth will be higher than that of this year. The semiconductor market is also cyclical, so it will be impacted by global GDP growth this year.

Finally, how does the research firm forsee Nymonyx (there was an article saying it will conquer NAND Flash)?

According to Kim, Numonyx is still a major NOR flash supplier with limited NAND flash market share. Unlike Intel, Numonyx’s focus is on mobile applications. Its joint-venture partner, Hynix, is scaling down its NAND flash production at this time and is focusing on DRAM production.

iSuppli doesn’t expect Numonyx to be a formidable competitor in the NAND flash memory market during the near term.

Top 20 global semicon companies — DRAM, Flash suppliers drop out

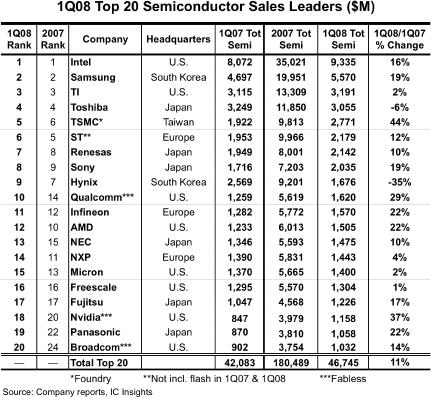

IC Insights recently published the May update to The McClean Report, featuring the Top 20 global semiconductor companies. Not surprisingly, there have been some significant movers and shakers. The most telling — quite a few of the major DRAM and Flash suppliers have dropped out of the Top 20 list!

First the movers! Fabless supplier Qualcomm jumped up four spots, ranking as the 10th largest semiconductor supplier in Q1-08. Next, Broadcom, the third largest fabless supplier, also moved up four positions, up to the 20th position. Panasonic (earlier, Matsushita), moved up to the 19th position, while NEC of Japan moved up to the 13th position.

First the movers! Fabless supplier Qualcomm jumped up four spots, ranking as the 10th largest semiconductor supplier in Q1-08. Next, Broadcom, the third largest fabless supplier, also moved up four positions, up to the 20th position. Panasonic (earlier, Matsushita), moved up to the 19th position, while NEC of Japan moved up to the 13th position.

TSMC, the leading foundry, moved up one position, registering the highest — 44 percent — year-over-year Q1-08 growth rate, besides being ranked 5th. Nvidia, the second largest fabless supplier, was another company registering a high YoY growth rate of 37 percent, and moved into the 18th position. Some others like Infineon, Sony and Renesas also climbed a place higher each, respectively. The top four retained their positions — Intel, Samsung, TI and Toshiba.

And now, the shakers! The volatile DRAM and Flash markets have ensured the exit of several well known names such as Qimonda, Elpida, Spansion, Powerchip, Nanya, etc., from the list of the top 20 global semiconductor companies, at least for now.

Among the others in the list, the biggest drops were registered by NXP, which dropped to 14th from 11th last year, and AMD, which dropped two places, from 10th to 12th. Two memory suppliers — Hynix and Micron — also slipped two places, to 9th and 15th places, respectively. STMicroelectronics also slipped from 5th to 6th. IBM too slipped out of the top 20 list.

The top 20 global semiconductor firms comprises of eight US companies (including three fabless suppliers), six Japanese, three European, two South Korean, and one Taiwanese foundry (TSMC). Also, looking at the realities of the foundry market, TSMC’s lead is now unassailable. If TSMC was an IDM, it would be No. 2, challenging Intel and passing Samsung, said one analyst, recently, a thought shared by many.

IC Insights has reported that since the Euro and the Yen are strong against the dollar, this effect will impact global semiconductor market figures when reported in US dollars this year.

There are some other things to watch out for. Following a miserable 2007, the global DRAM module market is likely to rebound gradually in 2008 due to the projected recovery in the overall memory industry, according to an iSuppli report. That remains to be seen.

Some new DRAM camps — such as Elpida-Qimonda, and Micron-Nanya — have been formed. It will be interesting to see how these perform, as will be the performance of ST-backed Numonyx.

Further, the oversupply of NAND Flash worsened in Q1-08, impacted by the effect of the US sub-prime mortgage loan and a slow season, according to DRAMeXchange. The NAND Flash ASP fell about 35 percent compared to Q4-07. Although the overall bit shipment grew about 30 percent compared to Q4-07, the total Q1-08 sales of branded NAND Flash makers fell 15.8 percent QoQ to US$3.24bn. Will the NAND Flash market recover and by when?

New camps promise exciting times ahead in memory market

The last few weeks of this month witnessed some interesting developments in DRAM. No, there are not signs of a recovery, yet. Instead, the appearance of new DRAM camps, as well as a new memory interface working group, does generate some interest.

However, first, the stats. DRAMeXchange recently reported that the Q1-08 revenues of the branded DRAM makers, impacted by continual low DRAM prices, fell by roughly 5.8 percent compared to Q4-07. Likewise, the contract prices and the spot prices fell 19 percent and 11 percent respectively.

DRAMeXchange further reported that barring Elpida and Powerchip, all other DRAM makers experienced a decline in revenues. Both Elpida and Powerchip witnessed slight increase in their market share during Q1-08.

Categorizing the DRAM industry market share by countries, Japan only increased by 0.9 percent from 13.5 percent to 14.4 percent, as Elpida’s revenue increased in Q108. Taiwan’s share increased by only 1.1 percent from 13.6 percent to 14.7 percent, as Powerchip gained market share. Korea sustained the same market shares — 47.2 percent, as in Q4-07.

However, America and Germany lost share. America’s share slipped from 13.6 percent to 13 percent, while Germany’s share fell from 12.2 percent to 10.8 percent, respectively.

In a recent investor conference, Samsung announced it will increase its Bit Growth Rate from 70 percent to 100 percent, an indication of its desire to continue reigning as a DRAM market leader.

Now, to the really interesting developments. First, Nanya and Micron signed an agreement to create MeiYa Technology Corp., a new DRAM joint venture. One of Nanya’s 200mm facility in Taiwan will be upgraded to 300mm starting this year, with the facility going online for production in 2009. Besides MeiYa, Nanya and Micron will co-develop and share future technology.

If this wasn’t enough, close on the heels of the Micron-Nanya JV, Elpida Memory and Qimonda AG, signed a Memorandum of Understanding (MoU) for a technology partnership for jointly developing memory chips (DRAMs), and accelerate their roadmap to DRAM products featuring cell sizes of 4F2.

Analysts at DRAMeXchange believe that the Qimonda-Elpida alliance re-shuffles the DRAM competitive landscape. It is also a sign of Qimonda’s determination to develop stacked process.

Lastly, ARM, Hynix Semiconductor Inc., LG Electronics, Samsung Electronics, Silicon Image Inc., Sony Ericsson Mobile Communications AB, and STMicroelectronics announced the formation of a working group, the Serial Port Memory Technology (SPMT), which is committed to creating an open standard for next-generation memory interface technology targeting mobile devices.

SPMT, a first-of-its-kind memory standard for DRAM, is said to enable an extended battery life, bandwidth flexibility, significantly reduced pin count, lower power demand and multiple ports by using a serial interface instead of a parallel interface commonly used in today’s memory devices.

Handset vendors have joined the fray as this technology will not only extend battery life, it will allow high-performance media-rich applications as well, that are likely to be the norm on next-generation mobile phones.

Surely, these developments and the emergence of new camps promise some exciting times ahead in the memory market.