Archive

Congrats TSMC, for raising R&D spend! But, what about Indian firms?

Source: IC Insights, USA.

Congratulations to TSMC for making it to the top 10 R&D spenders during 2010! If you look at the IC Insights’ table (see here), you’d understand what I am referring to!

First, the table itself. It has no major surprises, barring TSMC, which again is not really a surprise. As IC Insights itself says, “The industry is increasingly dependent on the success (and hopefully not, failure) of the foundries to continue advancing their IC manufacturing capabilities.”

TSMC has jumped up from 19th to the 10th place in the latest R&D spend. IC Insights expects that TSMC’s R&D spending in 2011 will grow another 20 percent, putting its budget over $1.1 billion for the year.

Otherwise, the top 9 in the list consist of Intel, Samsung, ST, Renesas, Broadcom, Toshiba, Qualcomm, TI and AMD — all big, strong players. However, TSMC, is the only foundry in that list, at the 10th spot.

Now, all of this makes great reading! Everyone connected with the global semiconductor industry is very well aware of TSMC’s strengths and capabilities.

The more TSMC grows in stature, the more will its capabilities grow. A lot of firms have already exited the manufacturing industry, leaving that to the likes of TSMC and others, and some more are due soon.

However, I am thoroughly disappointed by some folks who touch upon India missing out on the R&D story. More of that in a bit!

First. where is the R&D strength of India? There are firms, based outside the country, managed by Indians, who seem to look down on the country. I even received an email from a gentleman, which says: ‘Without semiconductors, India cannot gain technological advantage. Semiconductor should be funded by the defense budget.” I am appalled!

Well, we are trying, aren’t we? There are names that come to the mind — Procsys, Ittiam, SoftJin, eInfochips, MindTree, and so on! Yes, I know they aren’t exactly world beaters. But hey, they are all doing their own thing reasonably well!

Top 20 global semicon companies — DRAM, Flash suppliers drop out

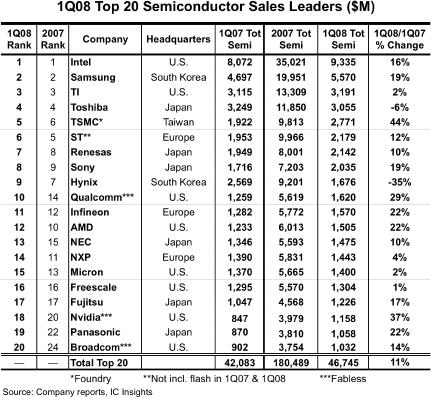

IC Insights recently published the May update to The McClean Report, featuring the Top 20 global semiconductor companies. Not surprisingly, there have been some significant movers and shakers. The most telling — quite a few of the major DRAM and Flash suppliers have dropped out of the Top 20 list!

First the movers! Fabless supplier Qualcomm jumped up four spots, ranking as the 10th largest semiconductor supplier in Q1-08. Next, Broadcom, the third largest fabless supplier, also moved up four positions, up to the 20th position. Panasonic (earlier, Matsushita), moved up to the 19th position, while NEC of Japan moved up to the 13th position.

First the movers! Fabless supplier Qualcomm jumped up four spots, ranking as the 10th largest semiconductor supplier in Q1-08. Next, Broadcom, the third largest fabless supplier, also moved up four positions, up to the 20th position. Panasonic (earlier, Matsushita), moved up to the 19th position, while NEC of Japan moved up to the 13th position.

TSMC, the leading foundry, moved up one position, registering the highest — 44 percent — year-over-year Q1-08 growth rate, besides being ranked 5th. Nvidia, the second largest fabless supplier, was another company registering a high YoY growth rate of 37 percent, and moved into the 18th position. Some others like Infineon, Sony and Renesas also climbed a place higher each, respectively. The top four retained their positions — Intel, Samsung, TI and Toshiba.

And now, the shakers! The volatile DRAM and Flash markets have ensured the exit of several well known names such as Qimonda, Elpida, Spansion, Powerchip, Nanya, etc., from the list of the top 20 global semiconductor companies, at least for now.

Among the others in the list, the biggest drops were registered by NXP, which dropped to 14th from 11th last year, and AMD, which dropped two places, from 10th to 12th. Two memory suppliers — Hynix and Micron — also slipped two places, to 9th and 15th places, respectively. STMicroelectronics also slipped from 5th to 6th. IBM too slipped out of the top 20 list.

The top 20 global semiconductor firms comprises of eight US companies (including three fabless suppliers), six Japanese, three European, two South Korean, and one Taiwanese foundry (TSMC). Also, looking at the realities of the foundry market, TSMC’s lead is now unassailable. If TSMC was an IDM, it would be No. 2, challenging Intel and passing Samsung, said one analyst, recently, a thought shared by many.

IC Insights has reported that since the Euro and the Yen are strong against the dollar, this effect will impact global semiconductor market figures when reported in US dollars this year.

There are some other things to watch out for. Following a miserable 2007, the global DRAM module market is likely to rebound gradually in 2008 due to the projected recovery in the overall memory industry, according to an iSuppli report. That remains to be seen.

Some new DRAM camps — such as Elpida-Qimonda, and Micron-Nanya — have been formed. It will be interesting to see how these perform, as will be the performance of ST-backed Numonyx.

Further, the oversupply of NAND Flash worsened in Q1-08, impacted by the effect of the US sub-prime mortgage loan and a slow season, according to DRAMeXchange. The NAND Flash ASP fell about 35 percent compared to Q4-07. Although the overall bit shipment grew about 30 percent compared to Q4-07, the total Q1-08 sales of branded NAND Flash makers fell 15.8 percent QoQ to US$3.24bn. Will the NAND Flash market recover and by when?

NAND Q108 sales falls 15.8 percent

There’s a nice report today by DRAMeXchange on the state of the NAND Flash market. It is reproduced here.

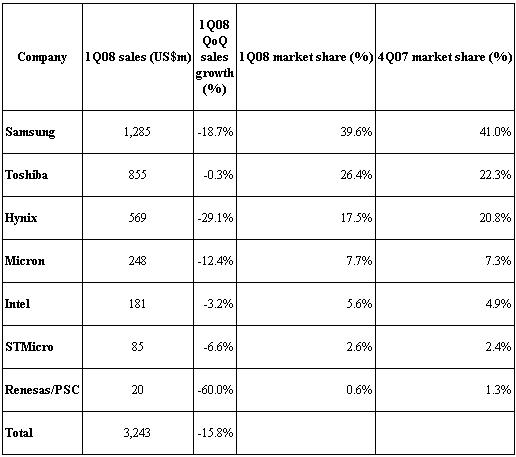

Impacted by effect of the US sub-prime mortgage loan and a slow season, oversupply of NAND Flash worsened in 1Q08. NAND Flash ASP fell about 35 percent compared to 4Q07. Although the overall bit shipment grew about 30 percent compared to 4Q07, the total 1Q08 sales of branded NAND Flash makers fell 15.8 percent QoQ to US$3.24bn.

Ranked by the overall 1Q08 sales, Samsung continues to lead. The top five NAND Flash branded makers shared 96.8 percent of the whole market share in 1Q08.

Ranked by the overall 1Q08 sales, Samsung continues to lead. The top five NAND Flash branded makers shared 96.8 percent of the whole market share in 1Q08.

Although the NAND Flash market share by sales for Samsung in 1Q08 fell to roughly 39.6 percent compared to 4Q07, Samsung continues to be the leader in branded market.

Despite the increase proportion of 51nm node production, affected by the deep decline in NAND Flash price, 1Q08 sales fell 18.7 percent QoQ to US$1.28bn.

NAND Flash market share by sales for Toshiba rose to 26.4 percent compared to 4Q07 and continued to be in the second place among the branded NAND Flash makers.

Due to Toshiba’s successful increase in 56nm node production, it was able to resist the effect of the NAND Flash price decline. However, 1Q08 sales were flat compared to 4Q07 at US$855m.

The 1Q08 market share by sales for Hynix fell to 17.5 percent, though it continued to stay at the number three spot among branded NAND Flash makers. As Hynix lowered its NAND Flash production, 1Q08 bit shipment increased only 9 percent QoQ. However, due to the fall of NAND Flash ASP at 39 percent QoQ, 1Q08 sales for Hynix fell to US$569m, or a decline of 29.1 percent QoQ.

With the ramp up of 50nm node, Micron and Intel continued to see steady growth in a bit shipment in 1Q08. However, impacted by the large decline in NAND Flash price, their 1Q08 sales fell compared to 4Q07. Micron and Intel 1Q08 sales were US$248m and US$181m, respectively, with a market share of 7.7 percent and 5.6 percent, each.

As STMicroelectronics primarily produces NAND Flash for cell phone applications, revenue for 1Q08 was not as severely impacted by the price decline. Revenue for STMicro in 1Q08 fell slightly to US$85m, or a slight decline of 6.6 percent compared to 4Q07. The 1Q08 market share by sales was 2.6 percent.

Since Renesas continued to reduce its AG-AND Flash production in 1Q08, Renesas/PSC camp sales fell roughly 60 percent compared to 4Q07 with a market share of 0.6 percent.

Top 10 semicon firms of 2007 by revenue

According to Gartner, the top 10 semiconductor firms for 2007 by revenue are: Intel, Samsung Electronics, Toshiba, Texas Instruments, STMicroelectronics, Infineon Technologies (including Qimonda), Hynix Semiconductor, Renesas Technology, NXP Semiconductors, and NEC Electronics.

Worldwide semiconductor revenue totaled $270.3 billion in 2007, a 2.9 percent increase from 2006, according to preliminary results from Gartner Inc.

Vendor performances were mixed with two vendors in the top 10 that experienced double-digit growth and two vendors that showed declines in revenue.

“Semiconductor vendors need to watch the performance of their end customers even closer as a major part of the industry becomes increasingly tied to consumer spending patterns,” said Andrew Norwood, research vice president at Gartner. “Loss of market share in an end-user application, such as a mobile phone, by a customer (a mobile phone manufacturer) can have a dramatic effect on a vendor’s business.”

Intel grew revenue more than twice as fast as the semiconductor market average, and it is likely to edge up its market share to 12.2 percent in 2007 from 11.6 percent in 2006.

Intel’s growth came primarily from strong shipments of mobile PCs. Armed with a strong product lineup for enthusiast desktops and servers, Intel regained lost share in those markets from AMD.

While the global market for dynamic random-access memory (DRAM) is expected to decline in 2007 due to a severe drop in prices caused by oversupply, Samsung Electronics is likely to increase its revenue by slightly higher than the overall global semiconductor market growth rate (DRAM is one the firm’s main products).

Samsung’s growth is driven by steady revenue growth in NAND flash memory and strong revenue growth in nonmemory areas such as application processors, media integrated circuits (IC), complementary metal-oxide semiconductor (CMOS) image sensor, smart card ICs and LCD driver ICs.

Toshiba’s revenue increased 27.8 percent in 2007 to $12,504 million, gaining three places in the rankings and moving into third place. The rapid gains mainly came from NAND flash memory.

Toshiba also increased production of CMOS image sensors for mobile phones and application-specific integrated circuits (ASICs)/application-specific standard products (ASSPs) revenue for digital consumer electronics, including LCD TVs, next-generation DVDs (HD DVDs) and video game consoles.

Major shakeups in top 10 semiconductor supplier rankings

According to the latest report from IC Insights, there have been major shakeups in the global top 10 rankings among suppliers of semiconductors.

Here’s what IC Insights has to say regarding some of the changes that took place in 3Q07:

* Toshiba rode the coat-tails of a 46 percent 3Q07/2Q07 NAND flash memory market surge to post an amazing 40 percent 3Q07/2Q07 semiconductor sales increase. This increase helped propel Toshiba to a third place ranking, its highest since being ranked as the second largest semiconductor supplier in 2000.

* AMD continues to display a nice recovery this year with its 3Q07 sales increasing 18 percent over 2Q07, which follows a 12 percent sequential increase in 2Q07/1Q07. As part of its continuing MPU marketshare battle with Intel, AMD is expected to announce a major manufacturing/foundry deal in the second half of 2007.

* The largest pure-play foundry in the world, TSMC, jumped one spot in 3Q07 as compared to the full-year 2006 ranking as the company recorded a strong 3Q07/2Q07 sales increase of 21 percent. It should be noted that after operating at only 83 percent capacity utilization in 1Q07, TSMC surpassed its “company-defined” 100 percent capacity utilization level in 3Q07!

* If pure-play foundry TSMC were excluded from the ranking, NXP would have been in the tenth position.

* In spite of 3Q07 DRAM pricing weakness, Hynix took advantage of its strong NAND flash marketshare to move from seventh to sixth place in the ranking.

* Freescale continues to feel the pain of its biggest customer, Motorola, as the company went from being ranked as the ninth largest semiconductor supplier in the world in 2006 to sixteenth in 3Q07. Unfortunately for Freescale, Motorola has gone from holding a 22 percent share of cellular phone unit shipments in 3Q06 (53.7 million) to securing only a 13 percent share in 3Q07 (37.2 million).

* TI, ST, and Renesas were the only top 10 companies to register less than double-digit 3Q07/2Q07 sequential sales growth rates. Each one of these companies is a top-10 supplier to the currently slow-growing analog IC market.

* The top 10 listing consists of three U.S., three Japanese, two Korean, one European, and one Taiwanese company.

Through the end of 2007, IC Insights expects to see pricing stability return to the DRAM memory market, surging IC demand for PCs and high-end cellular phones, and a continuation of the seasonal rebound in overall semiconductor demand that began in August.

Shifts in top 20 global semicon rankings

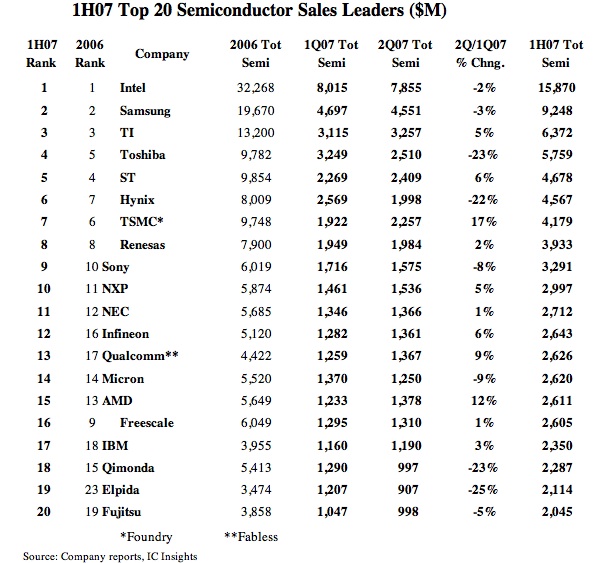

If the recent preliminary results released by IC Insights is anything to go by, there have been some movements among the top 20 semiconductor companies of the world during H1-2007. This is best illustrated by the table below.

While the top three — Intel, Samsung and TI, retain their positions, ST and Toshiba have exchanged the next two positions, as have Hynix and TSMC, while Renesas remains at no. 8!

Freescale has taken a big drop from no. 9 to no. 16, while Sony, NXP and NEC gained one place each. Infineon has climbed back up to no. 12, from no. 16, while Qualcomm occupies the no. 13 position, up from no. 17. AMD dropped two positions, from no. 13 to no. 15.

Will the semicon industry see a tight year ahead? As per reports, IC Insights said that there should be a “noticeable seasonal rebound” in overall IC demand beginning in September 2007, which may cause “significant changes” in the top 20 semiconductor ranking in the second half of 2007. Wait and watch this space!