Archive

Dexcel on growth drivers for Indian embedded design industry

It is my endeavor to write about semiconductors, solar/PV, EDA. FPGAs, embedded, etc., and related companies and solutions via this blog. One of the pleasures of writing a semicon blog is in being able to connect with and make a whole lot of friends from different countries, cultures, and companies, as well as bloggers.

One such gentleman is Ravinder Gujral or Ravi, as he’s popularly called, Director – Business Development, Dexcel Electronics Designs Pvt. Ltd. Dexcel, based very much in Bangalore, India, is among one of the emerging companies in the embedded space in the country. Ravi contacted me, like several others, via my blog! Likewise, I was elated to find myself a new friend and reader! Later, we met during Altera’s SOPC event, where Dexcel was exhibiting as well.

One such gentleman is Ravinder Gujral or Ravi, as he’s popularly called, Director – Business Development, Dexcel Electronics Designs Pvt. Ltd. Dexcel, based very much in Bangalore, India, is among one of the emerging companies in the embedded space in the country. Ravi contacted me, like several others, via my blog! Likewise, I was elated to find myself a new friend and reader! Later, we met during Altera’s SOPC event, where Dexcel was exhibiting as well.

Dexcel is an electronics design house with capabilities in embedded systems development, firmware Designs and development, DSP processors based designs, imaging software, device drivers, Linux porting, system level designs and development, application and automation software, development of audio and video codec, telecom related stacks, board designs and FPGA based digital designs services, and providing end-to-end solutions to customers.

Dexcel has an alliance and partnership with Altera (ACAP and DSP partner), and with Analog Devices (DSP collaborator), Texas Instruments (DSP third party Network Member), Actel (solution partner), Atmel (AVR 8-Bit RISC Consultants), Montavista Linux developer, etc. Quite impressive!

Estimate of Indian embedded industry

Naturally, our discussion veered toward embedded. Providing his estimate of the embedded design industry in India, Gujral said as per the survey conducted by the India Semiconductor Association (ISA) and Frost & Sullivan, the projected Indian semiconductor and embedded design industry will grow from $3.25 billion in 2005 to $14.42 billion in 2010 and to $43.07 billion in 2015. The Indian design organizations are moving beyond simple labor-cost arbitrage to become true contributors to product innovation.

Going forward, it is important to keep an eye on the drivers for embedded design. The main growth drivers for embedded software in the coming period will be mobile communications, military applications, networking devices and providing more intelligence and connectivity to consumer devices.

Gujral said: “The explosion of embedded devices is made possible mainly due to the rapid growth of semiconductor chips each year, and semiconductor devices becoming faster, cheaper and less power hungry. As the Indian domestic market is growing rapidly, this growth trend will continue. Simultaneously, there are technical challenges to design such products and services, and the availability of technical qualified resources has become more important.”

Localizing product designs and manufacturing

Given that India’s strength has been in embedded, would the biggest growth factor for embedded come from the localization of product design and manufacturing from India?

Indeed, it is! Gujral noted: “The growth factor for embedded companies will come from localization of product design and manufacturing from India. However, we should be doing well in localization of product design, rather than in manufacturing. Indian design engineers are strong in product innovation and design processes, while on the other hand, our manufacturing ecosystem is not as competitive as China.”

Going forward, India should be focused on fine tuning its design processes and best practices to become more efficient and productive, compared to counterpart in the US and Europe. “We have to develop strong domain technical knowledge to bring more innovation in product development,” added Gujral.

NI LabView solves embedded and multicore problems!

Some time ago, National Instruments (NI) introduced LabView 8.6. LabVIEW is a very data flow programming tool! And inherently, it has always been parallel processing!

Take note folks, as parallel is now increasingly becoming regular! And your multi-core problems could well be solved by NI’s LabView.

Given the ongoing recession, interestingly, NI projects double digit growth in 2009 for the region comprising India, Arabia and Russia. Jayaram Pillai, MD, India, Russia & Arabia, NI, says that these places have been traditionally strong in localization. The key is: what can NI’s technology bring in for indigenization!

Given the ongoing recession, interestingly, NI projects double digit growth in 2009 for the region comprising India, Arabia and Russia. Jayaram Pillai, MD, India, Russia & Arabia, NI, says that these places have been traditionally strong in localization. The key is: what can NI’s technology bring in for indigenization!

Pillai notes: “We have always talked about virtual instrumentation. How can you bring the local content into the system?” NI’s LabView’s ability has generally been to create a program out of a non-program. “Images are your natural language. We feel engineers can express themselves using graphical language,” he adds.

LabView inherently meant for parallel programming

Most embedded systems provide quick and easy solutions. NI is trying to put electronics into every problem that it confronts. About 98 percent of the processing environments are used elsewhere, other than the PCs. What embedded can do today is tremendous! NI’s LabView is inherently meant for parallel programming.

Pillai says: “When you are running two cores, it is important how you share the data between the cores. We have multi-core for Windows. We can do multi-core programming for embedded as well.” NI’s tools perform multi-core programming, which itself is a software program.

Besides targeting particular silicon and other resources, there are other problems or areas to deal with, such as test maths, state chart and data flow programming, etc. NI has built all of these components into LabView 8.6 — things such as programming MCUs, FPGAs, Power PCs, etc., can be handled.

Solve embedded problems by developing simpler systems!

Coming back to embedded systems, there are two requisite steps — programming the electronics and programming the system. “We see ourselves getting into the space of solving multi-core problems,” adds Pillai. “Everything today is software enabled. We intend doing for T&M what spreadsheet has done for financial analysis.”

Definitely, software is the instrument in virtual instrumentation. “It means, to solve 98 percent problems of the embedded applications, there is a need to make the development of embedded systems even simpler,” he contends, and rightly so!

“As we went higher in abstraction, we found that we were able to solve more problems. You’ve got to get into a high level of abstraction, which can be done by LabView, called system design platform. LabView today, is the platform for test and embedded,” notes Pillai.

In grahical system design, there is a need to leverage and collaborate in parallel. Graphical programming harnesses multi-core processors. LabView has also been the runaway software tool for DAQ and instrument control. As a result, more and more people can now do embedded programming.

Pillai advices: “If you want to build systems, you need to integrate NI design tools with third-party design tools to share the data. The integration of data has to be seamless.”

Benefits of graphical system design

Graphical system design should do for embedded what PCs did for desktops. “We are a graphical design company and are now building systems,” he adds. The concepts of graphical system design include design, prototype and deploy.

So, what are the product lifecycle benefits of graphical system design? There are multiple hardware systems priced at different cost points based on performance. A LabView user can install the software into an expensive system for testing purposes, and later, deploy on to a lower platform.

Legacy problem and major paradigm shift

Sharing of data between cores is key! Parallel programming in sequential does not make sense. Rather, data flow programming makes a lot of sense. However, there is a legacy problem as far as multi-core programming is concerned. That is: how do you shift so much of the sequential programming knowledge into data flow? This will require a major paradigm shift.

Besides, there are a lot of sequential tools as well. There is a need to integrate all of that into multi-core. So far, multi-core problems have been addressed in test and embedded systems. It is still on in gaming, though! Maybe, this too will be cracked in a matter of time!

To all of my Chinese friends, Kung Hei Fat Choy!

Embedded computing — 15mn devices not so far away!

It has been close to three weeks since the Intel IDF @ Taipei, Taiwan. However, way too many things happened there, which still deserve a mention. One such event would be the keynote on embedded Internet by Doug Davis, Intel’s Vice President, Digital Enterprise Group and General Manager, Embedded and Communications Group.

It has been close to three weeks since the Intel IDF @ Taipei, Taiwan. However, way too many things happened there, which still deserve a mention. One such event would be the keynote on embedded Internet by Doug Davis, Intel’s Vice President, Digital Enterprise Group and General Manager, Embedded and Communications Group.

Today, there are 5 billion connected devices, and this number should likely go up to 15 billion by 2015, as per IDC. However, technology barriers need to be overcome. Davis cited these challenges as reliability and long life, software scalability, low power and low cost, privacy and data security, IPv4 addressing and open standards. As of now, the Intel architecture (IA) is said to be (due to lack of any good competition) the preferred architecture for the embedded Internet.

While on embedded products, post the Intel Atom processor, Davis said that the Menlow XL is likely for a Q1-09 introduction. The associated market segments include retail, PoS, digital signage, kiosks, vending, ATM, etc.

On digital PoS for retail markets, Davis highlighted India, and rightly so, adding that digital retail PoS would find applications, given the growing and quite affluent Indian middle class. Such a digital PoS device could improve inventory management and transaction security, allow more efficient space utilization, etc. Yet another application is digital signage for business intelligence [as informative displays].

Davis showed all of us MediaCart’s example. MediaCart is providing a unique shopping experience. It is trying to revolutionize the shopping experience with a computerized shopping cart that assists shoppers, delivers targeted communications at the point of purchase, and streamlines store operations. Incidentally, Singapore’s Venture GES was contracted by MediaCart to develop the new shopping experience cart.

Pervasive embedded computing

Davis believes that embedded computing would become more pervasive in the days ahead. “The Intel architecture has all of the unparalleled scalability to meet these needs,” he added.

Davis estimated that China could go on to become the world’s largest semiconductor market over the next five years or so. Semiconductor TAM for industrial automation is likely to grow from $13.5 billion in 2008 to $17.5 billion in 2012. India is said to be the second largest destination for industrial automation, which is interesting, and something to look forward to.

Digital factory

We have all had some visions, sometimes of how a digital factory would look like? And, who would be working at such a factory. Possibly, robots, or industrial robots would make up the attendance!

Well, if KUKA, a company that builds the world’s leading robotic and automation devices is to be believed, we are a little closer than before to this vision or dream. Bruno Geiger, managing director, Asia Pacific, KUKA, pointed out in his chat with Davis that the company makes robotic and automation devices based on Intel’s platorms. That, ‘takes us closer to the vision of a digital factory!’ This is a great example of multi-core in industrial automation.

Portal for embedded designers

Getting back to the embedded Internet, Davis said that the greatest challenge for customers is to integrate new technologies. To address this need, Intel is investing in a new Web portal for embedded designers. He announced that the Intel Architecture Embedded Design Center, a Web portal for embedded designers, will likely get launched in the spring of 2009. This is indeed something to look forward to!

Asia has all the trappings to become the largest market for embedded computing, and Taiwan, the largest market for automation. Well, don’t count India out! Embedded systems and software is India’s strength, and don’t be surprised to see and hear about lots of such activities from the country.

No fabs? So?? Fabless India shines brightly!!

This is no secret: fabs or no fabs, fabless India has been shining brightly all this while and will continue to do so for some time!

I’ve blogged on numerous occasions about India’s strength in design services, India as the embedded superstar, and well, about India’s growing might in global semicon. A fab will surely boost India’s image on the global map, but it is definitely not that essential!

It was very pleasing to hear S. Janakiraman, former chairman, India Semiconductor Association, and President and CEO-R&D Services, MindTree, also highlight this fact at Altera’s SOPC conference recently. Perhaps, India has been emphasizing on having a fab. However, if the fabless segment keeps growing as it has been up until now, that would boost industry growth as well!

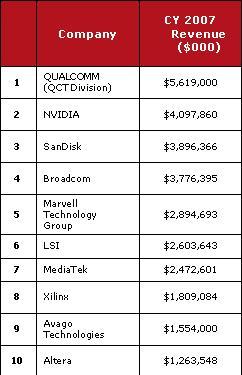

Top 10 global fabless companies For the record, here are the top 10 global fabless companies of the world, as reported by the Global Semiconductor Alliance (GSA), formerly, Fabless Semiconductor Association, USA.

For the record, here are the top 10 global fabless companies of the world, as reported by the Global Semiconductor Alliance (GSA), formerly, Fabless Semiconductor Association, USA.

According to GSA, the total fabless revenue was $27.3 billion, a 12 percent growth year-on-year during 1H 2008. I believe, quite a few, or nearly all of the companies within the GSA top 10 list, have some sort of a presence in India!

Let’s also re-visit the numbers provided by ISA-Frost & Sullivan in its study on the Indian semiconductor industry. The India semiconductor TAM (total available market) revenues will likely grow by 2.5 times, and the TM (total market) will likely double revenues in 2009. Is this not good enough?

Bear in mind that India also plays an active role in the verification and software domains, and it is increasingly covering the entire design chain. The fabs. vs. fabless debate has been going on since 2004-05. Back then, too, many industry observers were backing the fabless route. Now, this discussion is perhaps, a non-issue, with the fabless segment easily the star performer.

India has long had the expertise in chip/board design, embedded software and system engineering. Also, the product and service differentiation is being increasingly driven through software, where India already enjoys a lead over other the APAC countries.

India distinctly has a tremendous opportunity to lead the global market in both semiconductors and electronic products, with or without fabs, or even being fabless!

Yindusoft rocks embedded domain for India across Apac

India has, for long, been the acknowledged ’embedded superstar’ of the world! It is in no danger of losing that top position, especially in the near future, as several Indian firms in the embedded space continue to rock the world.

One such company is Yindusoft, established 2006, a software services company focused on the following domains: embedded software for IC design houses, OEMS/ODMS in consumer electronics; IT solutions in the semiconductor manufacturing sector; and distribute and customize higher end IT software products in the two areas.

G.K. Pramod, CEO, and a former member of Cybermedia/IDC said: “We are a two-year old company! We cover Asia Pacific especially, Taiwan and Singapore. We would like to expand into Korea and Japan, hopefully, by the end of Q4 2008.”

G.K. Pramod, CEO, and a former member of Cybermedia/IDC said: “We are a two-year old company! We cover Asia Pacific especially, Taiwan and Singapore. We would like to expand into Korea and Japan, hopefully, by the end of Q4 2008.”

Yindusoft is present in two domains: providing IT solutions to large semiconductor manufacturing companies, being the first. Pramod said: “We are working with companies like TSMC, UMC, etc. We work with them in CIM (computer-integrated manufacturing). We recently completed a project on wafer analysis in Taiwan. Our engineers developed the software to cut the wafers into precise shapes. We have onsite engineers with TSMC in Taiwan and UMC in Taiwan and Singapore. Now, we are aggressively positioned ourselves in the CIM space for semiconductors.”

The second important domain are OEMs/ODMs. Yindusoft develops embedded software for OEMs/ODMs. Pramod added: “We develop the software for these companies. In Taiwan, we have done work on digital signage systems. We worked on the UI design. We did development on the UI design itself, along with market research, and therefore, the customer received market feedback as well.”

Yindusoft has two recent design wins: designing of digital signage application for a large OEM/ODM in Taiwan. and designing of set-top box application for a large OEM/ODM in Asia Pacific.

Commenting further on Yindusoft’s design wins, he said: “We completed a large project in the area of digital signage product development with the help of an embedded product development domain expert. Our domain consultant adopted methods like market research, making global product feature list and getting the UI design development from design experts who are from art and design background (and, not IT background).”

Too early to estimate Indian semicon

Pramod added that it was quite early to estimate the strength of the Indian semiconductor industry as fabs are yet be commissioned for production. The Indian embedded design industry is estimated at $4-5 billion in 2008-09.

Commenting on the drivers for embedded design, Pramod said these could be the design capabilities of Indians and the requirement of low-cost consumer products. “Big markets like India and China would require lot of consumer devices for common man applications,” he said.

Customers expect strong domain expertise today. Definitely, and I completely agree on this,” he added. “We need domain expertise to speak the “customers’ language, make the project successful and show the differentiating factors in our service delivery.”

As mentioned, Yindusoft also works with the STB companies. “We are developing an STB (Set-top box) application. Typical applications would be PVR, email application, parental security, etc.,” he said.

Yindusoft is also trying out a model called offshore solutions center. Pramod said: “We have identified pain areas of customers, like OEMs/ODMs and semicon companies. Till such time the companies don’t develop the necessary software skills, there orders can get rejected. They can’t add value to their products. Therefore, profitability is a major issue with them. Next, they also have a language problem and cannot provide the essential technical support. Also, they cannot enter the Indian semiconductor market because of these reasons.

“Hence, we are now trying to build up a solution for them. One is the ODC, which is regular. The second factor: localization of their product for the Indian market, is an example. We also have a demo center. We conduct the market research for a particular product and then set up a demo center in India for that product. After that, there’s the technical support center.”

Way forward for embedded

Would the biggest growth factor for embedded come from localization of product design and manufacturing from India? What’s the way forward?

Pramod said that the biggest growth factor for embedded could come from the localization of product design, and it will be the driving factor. “In fact, we provide this as a value addition to our customer, he added. “Indians need to focus on designs, which is our core strength.” However, he felt that China would still lead in manufacturing.

Finally, what did the Indian semiconductor industry offer to the world, and why should the others should come here?

Pramod listed six key capabilities: Design capabilities of Indians; VLSI design, IC design capabilities; software integration capability; good software knowledge; India is also a good pilot market to launch new embedded products; and India is a strategic location for Asia Pacific markets where there is a good ecosystem for the semiconductor industry.

The company’s head office is located in Bangalore, while it has two overseas offices in Taiwan and Singapore, respectively.

Yindusoft’s vision is to be the leaders in providing software services for IC design houses, OEM/ODMS and semiconductor manufacturing companies.

The mission is to act as a software consultant in new product development by providing cost effective co-working models and establish offshore solution centers (OSC) in India. Best of luck!