Archive

Top 20 semicon rankings Q2-09 — TSMC climbs up, AMD slips down!

Very interesting, isn’t it? And I am not surprised! TSMC deserves to move up the top 20 semiconductor companies rankings!! It seems that AMD especially needs to really get its act together.

First, to the rankings. Recently, IC Insights released the list of the top 20 semiconductor sales leaders during Q2-09. Source: IC Insights

Source: IC Insights

In this list, there are four fabless semiconductor companies — Qualcomm, Broadcom, MediaTek and Nvidia in the top 20, and one foundry — TSMC, perhaps, emphasizing the growing influence of TSMC as well as the fabless semiconductor companies.

AMD slips! Again?

I had written a couple of posts some time back on AMD and Intel, where the former had commented on the EC ruling on Intel, and also how both were at each other’s throats, and had asked the question — how will all of this help the market?

Well, one hopes that AMD will come back very much stronger in the next quarter, despite its uninspiring guidance for 3Q09, saying that it expects its sales to be “up slightly” from 2Q09.

TSMC, Hynix, MediaTek shine

Coming back to the table, the clear movers are TSMC, and no surprises there, as well as Hynix and MediaTek. In fact, with a little better Q3 performance, TSMC could well move up to the third position, overtaking both Texas Instruments and Toshiba.

Look at the last column — the 2Q09/1Q09 percentage change — TSMC has grown by a whopping 93 percent! One other thing! TSMC is reportedly eyeing business opportunities in solar photovoltaics and LEDs in a bid to diversify its revenue channels. Should these happen, expect TSMC to move up higher!

The closest to TSMC in terms of growth are Hynix at 40 percent and Qualcomm at 36 percent, respectively. MediaTek, another impressive mover, grew by 20 percent. Of course, there is Samsung as well, with 29 percent growth.

ST, Micron, Nvidia and NXP have done well too! According to IC Insights, Nvidia replaced Fujitsu in the Q2-09 top 20 rankings. And that brings us to the shakers or those who fared poorly.

Fujitsu, AMD, Freescale slide!

I’ve already touched upon AMD. Fujitsu cited flash memory and automotive device sales to have suffered immensely this quarter. However, it hopes Q3 will be better and said that customer demand was picking up. So, it could well be back in the Top 20 during Q3.

Yet another slip was in store for Freescale. It slipped from 16th position in 2008 to 18th position during Q1-09, and slid further to 20th position in Q2-09. Perhaps, overdependance on automotives has been its undoing.

An interesting statistic from IC Insights — Fujitsu, with -9 percent and Freescale, with -2 percent growth, were the only two top-20 companies from Q1-09 to register a 2Q09/1Q09 sales decline!

Wonderful industry guidance

It is heartening to see 19 of the 20 companies registering positive growth this quarter. It won’t be improper here to commend IC Insights on its wonderful industry guidance!

In an IC Insights study from late December 2008, it was very vocal in advising firms to adopt a quarterly outlook! It also forecast a significant rebound in the IC market beginning in the third quarter of the year!

IC Insights also stood out by pointing out in early July that H2-09 is likely to usher in strong seasonal strength for electronic system sales, a period of IC inventory replenishment, which began in 2Q09, and positive worldwide GDP growth.

IC Insights had marked 4Q08 as the beginning of the downturn/collapse and Q1-09 as the bottom of the cycle. This quarter (Q2) has largely been a replenishment phase for the inventories. Going by that count, Q3 could well see a true seasonal increase in demand. IC Insights also said that during Q4-09, market growth will mirror the health of the worldwide economy and electronic system sales.

There is light, after all, at the end of the tunnel! Wonder why are the industry folks continue to tell each other — we still aren’t having a good time! Maybe, it is time for them to shed their pessimism and from holding back on investments, and move on to show steely optimism, and indulge in really aggressive buying and selling! After all, work and progress will happen ONLY if you work!!

Intel's margins hurt again by Atom to tune of $1bn

Intel’s misjudgment of the low margins of the Atom in its netbook processor has hurt the company for the second successive quarter, according to the report: “Netbook-Mobile Internet Device Convergence: Strategic Issues and Markets,” recently published by The Information Network (www.theinformationnet.com).

The Information Network had stated on January 7 that Intel misjudged the success of the Netbook and its Atom processor to the tune of about a billion dollars for Q4. Given the low margins announced in its Q1 release, Intel is still bogged down by the Atom.

The Atom used in a Netbook is processed with 45nm feature sizes on 300mm wafers and measures 25sqmm. It is priced at about $29. Intel’s Penryn Core 2 processor is used in Notebooks. It is also processed with 45nm feature sizes on 300mm wafers and measures 107sqmm. It is priced at about $279. There is a price difference of $200 per processor between the Penryn and Atom, but more importantly, a difference of $115,000 per processed 300mm wafer.

“Intel rethought its production schedule in Q1 by allocating capacity for the Atom and for the Penryn, unlike Q4 where the cut back production on the more profitable Penryn,” noted Dr. Robert N. Castellano, president of The Information Network. “We estimate that Intel produced 5 million Atom processors and 50 million Penryns.”

On March 2, Intel and TSMC announced they had reached an agreement to collaborate on technology platform, IP infrastructure, and SoC solutions for the Atom CPU cores. That situation will improve Intel’s margins for Q2 2009.

“While the announcement was slated toward TSMC’s capability to produce Atom cores for Intel’s march into the Mobile Internet Device (MID) market, which is dominated by ARM, it was an opportunity for Intel to wipe production of the Atom off its books. I’d like to think of it as ‘Intel’s Atom Bomb’,” added Dr. Castellano. “It indicates the tech sector is not really that bad off as the numbers suggest, but just a miscalculation on Intel’s part. Indeed, Intel did say that the bottom had been reached in the PC sector.”

Yindusoft rocks embedded domain for India across Apac

India has, for long, been the acknowledged ’embedded superstar’ of the world! It is in no danger of losing that top position, especially in the near future, as several Indian firms in the embedded space continue to rock the world.

One such company is Yindusoft, established 2006, a software services company focused on the following domains: embedded software for IC design houses, OEMS/ODMS in consumer electronics; IT solutions in the semiconductor manufacturing sector; and distribute and customize higher end IT software products in the two areas.

G.K. Pramod, CEO, and a former member of Cybermedia/IDC said: “We are a two-year old company! We cover Asia Pacific especially, Taiwan and Singapore. We would like to expand into Korea and Japan, hopefully, by the end of Q4 2008.”

G.K. Pramod, CEO, and a former member of Cybermedia/IDC said: “We are a two-year old company! We cover Asia Pacific especially, Taiwan and Singapore. We would like to expand into Korea and Japan, hopefully, by the end of Q4 2008.”

Yindusoft is present in two domains: providing IT solutions to large semiconductor manufacturing companies, being the first. Pramod said: “We are working with companies like TSMC, UMC, etc. We work with them in CIM (computer-integrated manufacturing). We recently completed a project on wafer analysis in Taiwan. Our engineers developed the software to cut the wafers into precise shapes. We have onsite engineers with TSMC in Taiwan and UMC in Taiwan and Singapore. Now, we are aggressively positioned ourselves in the CIM space for semiconductors.”

The second important domain are OEMs/ODMs. Yindusoft develops embedded software for OEMs/ODMs. Pramod added: “We develop the software for these companies. In Taiwan, we have done work on digital signage systems. We worked on the UI design. We did development on the UI design itself, along with market research, and therefore, the customer received market feedback as well.”

Yindusoft has two recent design wins: designing of digital signage application for a large OEM/ODM in Taiwan. and designing of set-top box application for a large OEM/ODM in Asia Pacific.

Commenting further on Yindusoft’s design wins, he said: “We completed a large project in the area of digital signage product development with the help of an embedded product development domain expert. Our domain consultant adopted methods like market research, making global product feature list and getting the UI design development from design experts who are from art and design background (and, not IT background).”

Too early to estimate Indian semicon

Pramod added that it was quite early to estimate the strength of the Indian semiconductor industry as fabs are yet be commissioned for production. The Indian embedded design industry is estimated at $4-5 billion in 2008-09.

Commenting on the drivers for embedded design, Pramod said these could be the design capabilities of Indians and the requirement of low-cost consumer products. “Big markets like India and China would require lot of consumer devices for common man applications,” he said.

Customers expect strong domain expertise today. Definitely, and I completely agree on this,” he added. “We need domain expertise to speak the “customers’ language, make the project successful and show the differentiating factors in our service delivery.”

As mentioned, Yindusoft also works with the STB companies. “We are developing an STB (Set-top box) application. Typical applications would be PVR, email application, parental security, etc.,” he said.

Yindusoft is also trying out a model called offshore solutions center. Pramod said: “We have identified pain areas of customers, like OEMs/ODMs and semicon companies. Till such time the companies don’t develop the necessary software skills, there orders can get rejected. They can’t add value to their products. Therefore, profitability is a major issue with them. Next, they also have a language problem and cannot provide the essential technical support. Also, they cannot enter the Indian semiconductor market because of these reasons.

“Hence, we are now trying to build up a solution for them. One is the ODC, which is regular. The second factor: localization of their product for the Indian market, is an example. We also have a demo center. We conduct the market research for a particular product and then set up a demo center in India for that product. After that, there’s the technical support center.”

Way forward for embedded

Would the biggest growth factor for embedded come from localization of product design and manufacturing from India? What’s the way forward?

Pramod said that the biggest growth factor for embedded could come from the localization of product design, and it will be the driving factor. “In fact, we provide this as a value addition to our customer, he added. “Indians need to focus on designs, which is our core strength.” However, he felt that China would still lead in manufacturing.

Finally, what did the Indian semiconductor industry offer to the world, and why should the others should come here?

Pramod listed six key capabilities: Design capabilities of Indians; VLSI design, IC design capabilities; software integration capability; good software knowledge; India is also a good pilot market to launch new embedded products; and India is a strategic location for Asia Pacific markets where there is a good ecosystem for the semiconductor industry.

The company’s head office is located in Bangalore, while it has two overseas offices in Taiwan and Singapore, respectively.

Yindusoft’s vision is to be the leaders in providing software services for IC design houses, OEM/ODMS and semiconductor manufacturing companies.

The mission is to act as a software consultant in new product development by providing cost effective co-working models and establish offshore solution centers (OSC) in India. Best of luck!

Top 10 global semicon predictions — where are we today

It is always interesting to write semicon blogs! Lots of people come up to me with their own comments, insights, requests, etc. One such request came from a friend in Taiwan, who’s involved with the semiconductor industry.

It is always interesting to write semicon blogs! Lots of people come up to me with their own comments, insights, requests, etc. One such request came from a friend in Taiwan, who’s involved with the semiconductor industry.

I was asked forthrightly what I thought of the top 10 global predictions, which I had blogged/written about some time back late last year.

Top 10 semicon predictions

For those who came in late, here are the 10 global predictions on semiconductors made at that time (late December 2007.

1. Semiconductor firms may have to face a recession year in an election year.

2. DRAM market looks weak in 2008.

3. NAND market will remain hot.

4. Power will remain a major issue.

5. EDA has to catch up.

6. Need to solve embedded (software crisis?) dilemma.

7. Consolidation in the fab space.

8. Capital equipment guys will continue to move to other market.

9. Spend on capital equipment to drop.

10. Mini fabs in developing countries.

Well, lot of water has flowed since those predictions were made. Let’s see how things stand, as of now. The updated predictions would look something like these:

1. There have been signs of recession, but the industry has faced it well, so far. In fact, Future Horizons feels that if there is going to be a global economic recession, the chip industry (but not all companies) is in the best shape possible to weather the ensuing storm.

2. Memory market is changing slightly as well, though people are very cautious. According to Converge, memory market prices appear to be stabilizing. iSuppli has predicted a poor year for DRAM though!

3. NAND Flash could show some recovery later this year. Yes, Q1-08 QoQ sales seems to have slipped, but the market remains hopeful of a recovery. Even iSuppli warned of NAND Flash slowdown in 2008, while Apple slashed its NAND order forecast significantly for 2008! Keep those fingers crossed!!

4. Power remains a big issue, and will continue to be so. This will remain as we move up newer technology process nodes.

5. EDA is seemingly catching up with 45nm designs. Magma, Synopsys, and the other leading EDA vendors are said to be playing big roles in 45nm designs.

6. Fabless companies are gaining in strength. No doubt about it! The 2007 semicon rankings show that. Also, Qualcomm is now the leader in the top wireless semicon suppliers, displacing Texas Instruments.

7. There have been consilidations (or long term alliances) in: a) fab space b) DRAM space. In the fab space, Intel, Samsung and TSMC have combined to go with 450mm wafer fab line by 2012. And in the DRAM space, there have been new camps, such as Elpida-Qimonda, and Nanya-Micron partnering to take on Samsung. With the global semiconductor market seeing steady decline in growth rate, which would continue, look forward to more consolidations.

8. Investments in photovoltaics (PV) have eased the pressure on capital equipment makers and spend somewhat. In fact, 2007 will be remembered as the year when the PV industry emerged as a key opportunity for subsystems suppliers and provided a timely boost in sales for those companies actively addressing this market. Perhaps, here lies an opportunity for India.

9. Mini fabs — these are yet to happen; so far talks only. In India, a single silicon wafer fab has yet to start functioning, even though it has been quite a while since the semicon policy was announced. Conversely, some feel that India should focus on design, rather than go after something as mature as having wafer fabs. However, several solar fabs — from Moser Baer, Videocon, Reliance, etc., are quite likely.

10. Moving to 45nm from 32nm is posing more design challenges than thought. This is largely due to the use of new materials. Well, 45nm will herald a totally different structure — metal gate/high-k/thin FET/deep trench design, etc. It will herald a new way of system design as well.

Now, I am not a semicon expert by any long distance, and welcome comments, suggestions, improvements from you all.

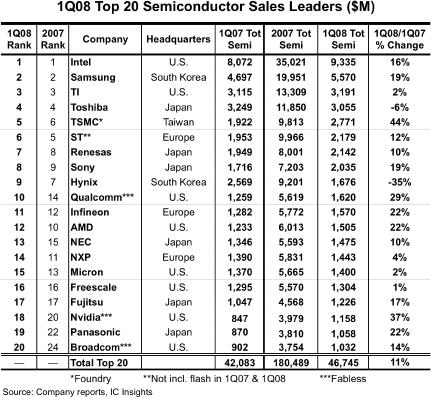

Top 20 global semicon companies — DRAM, Flash suppliers drop out

IC Insights recently published the May update to The McClean Report, featuring the Top 20 global semiconductor companies. Not surprisingly, there have been some significant movers and shakers. The most telling — quite a few of the major DRAM and Flash suppliers have dropped out of the Top 20 list!

First the movers! Fabless supplier Qualcomm jumped up four spots, ranking as the 10th largest semiconductor supplier in Q1-08. Next, Broadcom, the third largest fabless supplier, also moved up four positions, up to the 20th position. Panasonic (earlier, Matsushita), moved up to the 19th position, while NEC of Japan moved up to the 13th position.

First the movers! Fabless supplier Qualcomm jumped up four spots, ranking as the 10th largest semiconductor supplier in Q1-08. Next, Broadcom, the third largest fabless supplier, also moved up four positions, up to the 20th position. Panasonic (earlier, Matsushita), moved up to the 19th position, while NEC of Japan moved up to the 13th position.

TSMC, the leading foundry, moved up one position, registering the highest — 44 percent — year-over-year Q1-08 growth rate, besides being ranked 5th. Nvidia, the second largest fabless supplier, was another company registering a high YoY growth rate of 37 percent, and moved into the 18th position. Some others like Infineon, Sony and Renesas also climbed a place higher each, respectively. The top four retained their positions — Intel, Samsung, TI and Toshiba.

And now, the shakers! The volatile DRAM and Flash markets have ensured the exit of several well known names such as Qimonda, Elpida, Spansion, Powerchip, Nanya, etc., from the list of the top 20 global semiconductor companies, at least for now.

Among the others in the list, the biggest drops were registered by NXP, which dropped to 14th from 11th last year, and AMD, which dropped two places, from 10th to 12th. Two memory suppliers — Hynix and Micron — also slipped two places, to 9th and 15th places, respectively. STMicroelectronics also slipped from 5th to 6th. IBM too slipped out of the top 20 list.

The top 20 global semiconductor firms comprises of eight US companies (including three fabless suppliers), six Japanese, three European, two South Korean, and one Taiwanese foundry (TSMC). Also, looking at the realities of the foundry market, TSMC’s lead is now unassailable. If TSMC was an IDM, it would be No. 2, challenging Intel and passing Samsung, said one analyst, recently, a thought shared by many.

IC Insights has reported that since the Euro and the Yen are strong against the dollar, this effect will impact global semiconductor market figures when reported in US dollars this year.

There are some other things to watch out for. Following a miserable 2007, the global DRAM module market is likely to rebound gradually in 2008 due to the projected recovery in the overall memory industry, according to an iSuppli report. That remains to be seen.

Some new DRAM camps — such as Elpida-Qimonda, and Micron-Nanya — have been formed. It will be interesting to see how these perform, as will be the performance of ST-backed Numonyx.

Further, the oversupply of NAND Flash worsened in Q1-08, impacted by the effect of the US sub-prime mortgage loan and a slow season, according to DRAMeXchange. The NAND Flash ASP fell about 35 percent compared to Q4-07. Although the overall bit shipment grew about 30 percent compared to Q4-07, the total Q1-08 sales of branded NAND Flash makers fell 15.8 percent QoQ to US$3.24bn. Will the NAND Flash market recover and by when?

Semicon to grow 12pc in 2008: Future Horizons

If there is going to be a global economic recession, the chip industry (but not all companies) is in the best shape possible to weather the ensuing storm!

According to Malcom Penn, CEO, Future Horizons, we are dealing with a semiconductor industry in ‘deep trauma.’ He was delivering the company’s forecast at the recently held International Electronics Forum (IEF) 2008 in Dubai, predicting a 12 percent growth this year despite signs of a wobbling US economy.

According to Malcom Penn, CEO, Future Horizons, we are dealing with a semiconductor industry in ‘deep trauma.’ He was delivering the company’s forecast at the recently held International Electronics Forum (IEF) 2008 in Dubai, predicting a 12 percent growth this year despite signs of a wobbling US economy.

Is there a need to get back to the industry basics? “Semiconductors are a peculiar business; the only sane strategy is to bet the company regularly,” once remarked Dr Gordon Moore.

Penn noted that the current industry status is somewhat confused and uncertain. Short-term issues are dominating the agenda.

Longer-term structural trends are unclear. The traditional IDMs are currently going through a mid-life ‘new business model’ identity crisis, and the start-ups are struggling to even reach critical mass! And all of this has been happening amidst intense economic uncertainty

“Now is the time for strong nerves and determination,” Penn said. According to him, the underlying industry fundamentals are sound and there is no end in sight to the ‘make-lunch-or-be-lunch’ ethos.

The emerging economies like India and China have so far been less affected by the financial market’s turbulence. In fact, the emerging and developing economies were shifting the global growth dynamics.

Chip industry in best possible shape

A forecast health warning is: IF the global economy collapses, it will take the chip market with it. However, Future Horizons feels that if there is going to be a global economic recession, the chip industry (but not all companies) is in the best shape possible to weather the ensuing storm.

The ASPs are an enigma wrapped up in riddle. The course of ASPs (like love) never runs smooth. Wobbles happen! ASPs are also the perennial (and least understood) industry wild card. ASPs are generally driven by new IC designs, and that takes time (sometimes three to four years). Post-2001, value recovery lost one generation (130nm impact). The ASP recovery ‘wobbled’ in 2007 (memory and MPU price wars). Barring a recession, Future Horizons forecasts that ASPs will recover in 2008 (it has already started).

12 percent growth likely

Future Horizons’ 2008 forecast summary and assumptions (as of May 2008) are — ‘12 percent’ growth — ’10 percent’ units / ‘2 percent’ ASP. There may be no global economic recession, although US/UK/Eurozone might wobble — which they are! No significant inventory correction will probably take place, but there are always Q4>Q1 adjustments, and there’s nothing special about that either.

There could be lower fab capacity expansion due to 2007/2008 capex slowdown, which is inevitable and irreversible. There is also a possibility of a more stable memory price erosion — which means, back to the learning vs. bleeding curve, and prices have since hardened. If the global economy holds, the 2H-08 growth will likely be strong. This, if the capacity, ASP and units are all pulling together, which is said to be happening.

Therefore, Penn feels it is too early to call for a (major) downward revision. Q1 08 was a lot stronger than conventional wisdom feared.

“That’s the rational analysis, but semiconductors aren’t rational. It could just as easily be another single digit growth year,” Penn added.

Danger signs to watch out for

So, what are the danger signs one should watch out for? These would be capacity — it is hard to see how this can spoil 2008, provided unit growth holds up, but there is a need to watch capex. Another factor is demand — the current IC unit demand is sustainable provided the economy holds up, so there is a need to watch the inventory.

Next comes the economy! The current outlook continues to be uncertain with risks all on the downside. ASPs are the key to recovery, but always the first line of defence. ASPs could still derail 2008, but the trends are encouraging.

What’s driving the market?

In semiconductor 7.0 — or the 7th decade of the transistor revolution, the same things, as always, are driving the market. These are: technology, legislation — energy saving/conservation and structural — the relentless analog to digital conversion. All of these are combining to do what the chip industry does best — enabling something that was previously impossible. Penn contends, “This industry has nowhere near run out of steam!”

New applications continue to drive the market, with automotive, industrial and medical, mobile phones, and PCs and servers, dominating. The PC market is dominating, but going nowhere fast. Mobile phones have become more interesting, but have conflicting priorities. The challenges are: how to protect the existing cost structure and subscriber base and how to add useful and affordable value-add services! Evidently, “chipset suppliers love the high end, market loves the low end.”

There is definitely an increasing automotive semiconductor content. A solid annual growth has been prediced (CAGR 2006-11) for vehicles — 5.5 percent, systems — 11.5 percent, and semiconductors — 13.3 percent. Some other new areas are motor control and energy, as well as lighting and photovoltaic, besides medical electronics. Robotics is yet another interesting area.

Key industry issues

It is clear that more chips per wafer equals less cost per chip and more transistors per die equals more functionality. Several billion transistors gives phenomenal design flexibility as well. Considering total ICs and MOS ICs, in the MOS capacity build out by technology node, there has been no change in volume ramp profile despite the hype.

As for the evolution of the technology node, definitely, 45nm is a revolutionary step from 65nm. In all likelihood, 32nm will be a natural evolutionary. However, Penn cautioned that 22nm would be another ‘difficult’ transition!

There is no doubt that 65nm will be tomorrow’s leading-edge workhorse, having the same basic Si gate/SiO2/MOSFET structure. Nevertheless, 45nm will herald a totally different structure — metal gate/high-k/thin FET/deep trench design, etc. Also, 45nm will herald a new way of system design.

Is fabless right?

Is Fablite a valid option? While there is nothing wrong with being fabless, people are just not sure whether the best starting point is being an IDM. Teamwork has to be perfectly orchestrated as competition is tough.

As for the market share dynamics, the top 10 companies (IDMs) have been losing share. Fabless share has been growing, but it is still relatively small.

Coming to the realities of the foundry market, TSMC’s lead is now unassailable. Were it an IDM, it would be No. 2, challenging Intel and passing Samsung. Moving more into design looks inevitable.

Finally, execution, and not technology, is everything! Execution has and will continue to make the difference. Applications (software) will play the role of the key differentiator as well, and it has value. Design is the means to an end, and not the end.

From the chip industry’s perspective, the electronics market was traditionally Japan, North America and Western Europe. It now encompasses the entire Asian rim, China, Eastern Europe and India. Far from maturing, the chip industry itself is still in its volatile, high-growth phase, with at least a further 20 years of strong growth in prospect. Penn said, “The underlying growth drivers for chips has never been better.”

Back to basics

We started with the need to get

back to industry basics. We end in the same way! Stick to basics like:

* Don’t invest in low cost areas just because they are cheap — they have a habit of becoming high cost tomorrow, plus the hidden extras.

* Don’t make outsourcing decisions just because they are easy — especially if there’s no way back.

* Don’t make strategic cut-backs just to trim the bottom line — some decisions, e.g., R&D, take a long time to impact, then it’s too late.

* Stop looking for high volume/high value market niches — they don’t exist, need to learn how to compete

* Do show strong leadership

* Do have a long-term plan and stick with it — even if it negatively impacts ‘the next quarter’ balance sheet

* Do show a commitment and determination to succeed

* Do stay focused and resistant to external meddling

* Do execute ruthlessly — this is the key competitive differentiator)

* Do … just do it with passion — it’s the passion that makes the difference

Movers and shakers in semicon; new fabs in Asia

While speaking with the Fabless Semiconductor Association, USA, some time back, I quizzed them on the major movers and shakers (or slips) among the top 25, and what are the reasons for those.

Qualcomm has broken into the top 10 for the first time. It’s the first time in the history of semiconductors that such a thing has happened, and is probably a sign of the times ahead.

One reason for this growth has been — Increasing foundry orders. A Digitimes article reported that Qualcomm will increase orders by 15-20 percent in the September quarter to meet projections of strong 3G handset sales. According to the article, sources at Qualcomm suggest that wafer starts per month in the December quarter could surpass 30,000.

There have also been reports of strong June quarter for 2007. Qualcomm’s $2.32 billion in June quarter sales represents 19 percent year-on-year growth. Record chipset volumes of 65 million were at the high end of 62 million-65 million guidance. UMTS chipset shipments were noted to have increased by 127 percent year-over-year and 79 percent quarter-over-quarter, with the quarter-over-quarter growth rate roughly 4 times the market growth rate.

Finally, chipset ASPs increased by 2 percent year-over-year and quarter-over-quarter, and are likely to remain stable.

Situation in Asia

FSA quoted the Strategic Marketing Association’s Quarterly Spot Report – July. While there have been announcements in India by SemIndia, HSMC, Moser Baer, etc., for fabs, there is every likelihood of another fab in the eastern Indian state of West Bengal. The technology ministry announced plans for a yet to be named fab at the India Design Center. Another possibility is a fab in Kochi, South India, by the NeST Group.

In China, Strategic Marketing Association expects that eight new fabs will start construction this year. Two fabs have started construction in the first quarter (Hua Hong NEC and ProMOS), and two more have started construction in the second quarter.

Grace Semiconductor, now headed by former Infineon boss, Dr. Ulrich Schumacher, which opened its first fab in 2003, began moving equipment into the shell of Fab 2, which was built at the same time as Fab 1. The company is installing used equipment and plans to begin production in Q1 0f 2008. The company also plans to begin building a 300mm fab, perhaps as early as next year, although financing is said to remain an issue for such a project.

Also in China, IC Spectrum began building a 200mm fab in Kunshan, about 45km east of Shanghai. Using 0.35micron technology from Toshiba, the new foundry expects to begin volume production by the first quarter of 2009.

TSMC began production in the second phase of its 300mm Fab 14 in Tainan in the south of Taiwan. This $2.4 billion fab will start production at 65nm and move to 45nm in 2008. There are also plans for a 300mm Fab 14, Phase 3 at the same location.

Looking at capex

In 2007, companies with capital spending budgets of $1 billion or more (the Billion Dollar Club) will account for 77 percent of all capital spending. Most of these companies (13 out of 20) are memory companies. Nine of these companies are from Asia Pacific (South Korea, China, Taiwan and Southeast Asia). Together, they plan to spend $23 billion this year, more than half of what the Billion Dollar Club has budgeted for capital spending.

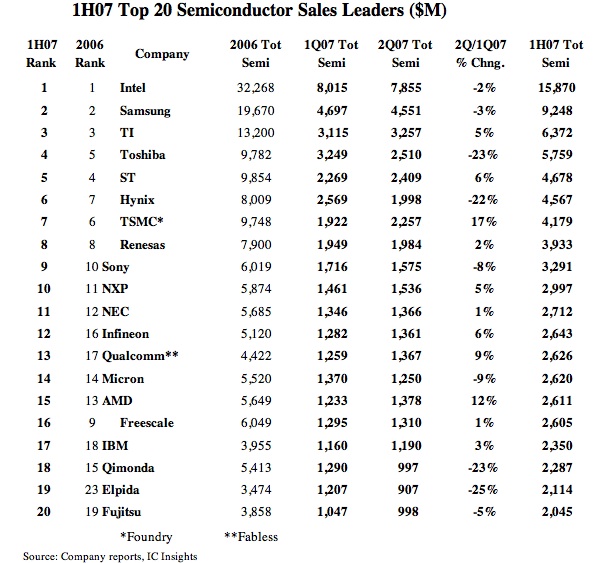

Shifts in top 20 global semicon rankings

If the recent preliminary results released by IC Insights is anything to go by, there have been some movements among the top 20 semiconductor companies of the world during H1-2007. This is best illustrated by the table below.

While the top three — Intel, Samsung and TI, retain their positions, ST and Toshiba have exchanged the next two positions, as have Hynix and TSMC, while Renesas remains at no. 8!

Freescale has taken a big drop from no. 9 to no. 16, while Sony, NXP and NEC gained one place each. Infineon has climbed back up to no. 12, from no. 16, while Qualcomm occupies the no. 13 position, up from no. 17. AMD dropped two positions, from no. 13 to no. 15.

Will the semicon industry see a tight year ahead? As per reports, IC Insights said that there should be a “noticeable seasonal rebound” in overall IC demand beginning in September 2007, which may cause “significant changes” in the top 20 semiconductor ranking in the second half of 2007. Wait and watch this space!